Do you know what are High book value low PE stocks?

Most investors hunt for cheap stocks. Very few hunt for the right kind of cheap.

There is a difference. A stock can be cheap because it is broken. Or it can be cheap because the market has simply stopped paying attention. The first kind destroys capital. The second kind builds it quietly, while everyone else is looking elsewhere.

This guide is built around finding the second kind. Specifically, stocks where the market price is below the company's actual net worth AND below what the sector is willing to pay for earnings. That combination, which is to say high book value paired with a low PE ratio, is what value investors call a Double Discount. It is rare. When it appears alongside clean debt and zero promoter pledging, it is worth paying serious attention to.

Here is everything you need to understand it, use it, and avoid the traps hiding inside it.

Related Reading from this section: Best high book value stocks in India

Imagine a company shut down tomorrow. It sold every factory, every machine, every piece of inventory. It paid off every loan. Whatever cash remained after all that would be divided among shareholders.

That remaining amount per share is the Book Value. Or as the formula states:

Book Value = (Total Tangible Assets - Total Liabilities) ÷ Outstanding Shares

The ratio that connects book value to the market price is the Price to Book ratio, otherwise known as the P/B ratio. When P/B is below 1, you are buying a rupee of real net assets for less than a rupee. You are buying the company for less than its liquidation value.

That is the starting point. But it is not enough on its own.

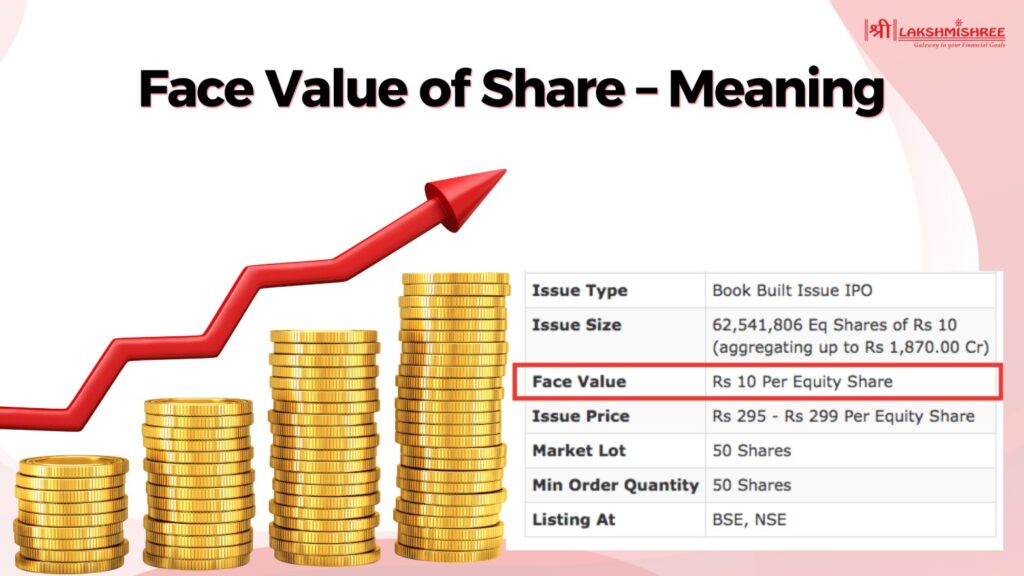

Most investors confuse "Book Value" with "Face Value." While book value tells you what a company owns, face value dictates its dividend math. To clear this confusion, read our:

book value tells you what a company owns.

face value dictates its dividend math.

Here is the mistake most investors make. They find a stock trading at 0.5x book value, assume it is cheap, buy it, and watch it do nothing for three years.

The problem is that book value tells you what the company was worth based on its assets. It tells you nothing about whether the company is actually making money today.

A factory sitting idle has book value. It generates no profit. Buying it cheap is not a bargain. It is a slow loss dressed up as a discount.

This is what value investors call a Value Trap: a stock that looks cheap on every metric but never recovers, because the cheapness is completely justified.

The fix is the PE ratio discussed in the next section before you get the list of best shares.

The PE ratio, which is to say Price divided by Earnings Per Share, tells you how many years of current profit it would take to recover your investment at today's price. A PE of 6 means six years of profit pays you back. A PE of 25 means twenty-five years.

Think of it like buying a small tea stall. The stall itself is worth Rs 50,000 in equipment and furniture. That is the book value. But if the stall earns Rs 20,000 profit every year and you buy it for Rs 50,000, your PE is 2.5. You recover your money in two and a half years. That is a genuine bargain.

If the stall earns nothing, the Rs 50,000 in furniture is just furniture. That is the trap.

Put both filters together, and you get the Double Discount: assets worth more than the price you pay, and earnings that recover your investment faster than the sector average. That combination is what every stock on this list had to clear.

Understand what CE and PE mean in the share market- click the image.

A low P/B and a low PE are necessary. They are not sufficient.

To separate genuine value from dangerous paper tigers, every stock here had to pass five conditions:

| Filter | Condition | What It Removes |

|---|---|---|

| P/B Ratio | Below 1.5 | Stocks priced above net worth |

| PE vs Industry | Below sector average | Relative overvaluation |

| Debt to Equity | Below 1.0 | Hollow book values built on loans |

| Promoter Pledging | Below 0.1% | Forced-sell crash risk |

| Net Profit | Positive | Hope stocks with no earnings floor |

The debt filter deserves a special note*

A company can have enormous assets on paper and still be essentially worthless to shareholders if those assets were built on massive loans. The bank is the real owner. Your book value protection only works if the company actually owns its assets outright.

The pledging filter is India-specific and critical. When promoters pledge their shares as collateral for personal loans, a stock market dip can trigger forced selling by lenders. That forced selling crashes the price further, triggering more forced selling. It is a spiral that hits minority shareholders hardest.

Every stock on this list has zero promoter pledging. That is not a coincidence. It was a hard requirement.

A low P/B and a low PE are necessary. They are not sufficient.

To separate genuine value from dangerous paper tigers, these 10 stocks had to pass these five conditions in this blog.

See also: PSU penny Stocks Below Book Value 2026 : government-owned names that pass similar screens.

All data from Screener.in, verified May 20, 2026

| Stock Name | CMP | P/B | P/E |

|---|---|---|---|

| Ashoka pipes | ₹129 | 0.87 | 3.47 |

| KNR Cons | ₹131 | 0.79 | 6.77 |

| PNC Infra | ₹219 | 0.85 | 13.71 |

| Maithan | ₹1,000 | 0.71 | 6.56 |

| Ruchira | ₹121 | 0.72 | 6.78 |

| Jindal Dril | ₹606 | 0.95 | 7.40 |

| GIC Re | ₹383 | 0.95 | 7.01 |

| Wim Plast | ₹365 | 0.79 | 7.28 |

| Prakash P | ₹188 | 0.98 | 11.20 |

| DCM Shriram | ₹41 | 0.40 | 8.93 |

Every single name here trades below its book value AND below its industry PE. That double discount appearing simultaneously across ten names in different sectors is exactly what this screen was built to find.

The government sector currently dominates the "Double Discount" list. To see which individual banks are leading this recovery, tap the image

These three names are on a temporary sale. Not a permanent one.

The market has pushed infrastructure stock prices down because government payments have been slow to arrive. Contractors finish roads, submit invoices, and wait. That waiting period compresses reported profits and frightens short-term investors away.

But here is what the quarterly headlines are hiding.

The order books of these companies are at three-year highs. The future revenue is already contracted. The ROCE, which is to say the return on every rupee of capital employed in the business, sits above 25% across the group. These are not struggling companies. They are healthy companies caught in a payment timing cycle that the market is misreading as a business deterioration.

Ashoka Buildcon is the most extreme example. Its PE of 3.47 against an industry PE of 18.2 represents an 81% discount. ROCE of 39.7%. Debt to equity of 0.47. Zero pledging. The profit compression is almost entirely explained by the Hybrid Annuity Model, which is to say a government payment structure where contractors build today and collect in guaranteed instalments over years. The cash is legally contracted. It simply has not been counted yet.

KNR Constructions adds a layer of protection the others do not have: irrigation projects alongside road contracts. That diversification means when NHAI payments slow, irrigation project billings continue. Two income streams rather than one creates a natural buffer that the market is currently ignoring entirely.

PNC Infratech is the conservative option in the group. Its discount to industry PE is narrower at around 25%, which is to say the market already partially recognises its quality. What it offers instead is geographic spread across UP, MP, and Rajasthan and cleaner billing cycles from state-run projects. Lower upside, lower surprise risk.

The infrastructure thesis connects directly to the broader government capex cycle covered in our PSU Fund guide. The same spending that powers PSU fund NAVs is what fills these companies' order books.

If the infrastructure group requires patience for a payment cycle to normalise, this group requires patience of a different kind, waiting for the market to notice what is already there simply.

Wim Plast has the widest valuation gap on the entire list. Its PE of 7.28 against a sector PE of 25.1 represents a 71% discount. The company makes plastic crates and material handling products for agriculture and logistics, which is to say it serves sectors with constant, repeat demand that does not disappear in economic downturns. The market ignores it because it is small and unglamorous. That inattention is precisely what creates the opportunity.

Prakash Pipes is the most debt-free name on the list with a debt to equity of 0.03. It trades at 0.98x book, which is to say near-liquidation pricing on a going concern business. Earnings have been compressed by high PVC resin input costs, but the demand driver, which is the Jal Jeevan Mission's multi-decade commitment to water access across India, has not changed. The product is still needed. The compression is temporary. The debt-free balance sheet means the company does not need profits to survive the wait.

GIC Re is a different kind of asset entirely. It is the insurance company for insurance companies, which is to say every insurer in India is legally required by IRDAI regulation to cede a portion of their premiums to GIC Re before doing business with anyone else. That is a regulatory moat that no private competitor can replicate. Yet the market prices it at 7x earnings against a sector average of 22.5x. The reason is catastrophe risk, i.e., one bad flood or earthquake quarter scares investors away. That fear creates the discount. The mandatory cession structure, which is permanent and government-mandated, creates the floor.

For context on government-backed value names like GIC Re, see our dedicated guide on High Book Value Government Stocks.

Low PE in commodity sectors normally signals a peak-earnings warning. The market is expecting profits to fall, which is why it refuses to pay a full multiple for current earnings. That caution is usually correct.

These three are exceptions, and here is the specific reason for each.

Maithan Alloys trades at Rs 1,000 against a book value of Rs 1,416. You are paying 71 paise for every rupee of assets. In the capital-heavy world of metal smelting, companies typically carry enormous debt. Maithan's debt to equity is 0.11. That near-zero debt load means when the global steel cycle eventually recovers, Maithan captures the margin expansion almost entirely for shareholders rather than surrendering it to interest payments. The company pays a dividend of 1.58% to keep you compensated while you wait.

Ruchira Papers has the most alarming headline number on the list: profit down 87%. But the paper market is going through a post-pandemic oversupply correction that is industry-wide, not company-specific. Ruchira's response to that downturn is what separates it from weaker peers: a 4.15% dividend yield, the highest income return on the entire list, paid out of balance sheet strength rather than operating earnings. Zero pledging. Debt to equity of 0.38. The company is paying you cash rent to wait for the cycle to turn.

Jindal Drilling operates in oil field services, which is to say it provides drilling rigs and technical services to ONGC and Oil India under long-duration contracts. The PE discount of 54% versus the sector exists because the market conflates oil field services with oil price risk. But Jindal's contracts fix revenue for years regardless of where crude trades on any given day. The rigs are contracted. The income is relatively stable. The market is applying the wrong fear to the wrong business.

This is the most important section. Read it before acting on anything above.

Three signs that a cheap stock is cheap for the right reasons:

Reliance Infrastructure appears on every high book value screener in India. P/B of 0.17. PE of 0.58. It looks like the deepest discount on any list.

It is not a discount. It is a warning.

| Metric | Value |

|---|---|

| CMP | Rs 71 |

| P/B | 0.17 |

| 1-Year Return | -73.90% |

| 3-Year Return | -20.42% |

| Debt/Equity | 0.34 |

The book value of Rs 413 against a price of Rs 71 implies an 83% discount. But that book value includes assets whose actual realisation in a distress scenario is significantly lower than stated. Multiple debt restructuring cycles, complex related-party structures, and a history of asset monetisation under financial pressure mean the stated book value is not a reliable floor.

Genuinely mispriced value stocks attract buyers as they fall toward book value. Reliance Infrastructure has not attracted that buying over years of decline. That is not an oversight by the market. It is a verdict.

Verdict: Excluded. The discount is warranted, not an opportunity.

For a detailed explanation of how debt restructuring distorts reported book value, see our NPA and Asset Quality Analysis Guide.

For investors specifically seeking the lowest financial risk combination on this screen:

| Rank | Company | D/E | P/B | Why It Qualifies |

| 1 | Prakash Pipes | 0.03 | 0.98 | Near-zero debt, Jal Jeevan Mission demand tailwind |

| 2 | Maithan Alloys | 0.11 | 0.71 | Structurally clean cyclical; BV 29% above CMP |

| 3 | Ashoka Buildcon | 0.47 | 0.87 | Conservative leverage; 39.7% ROCE |

| 4 | KNR Constructions | 0.49 | 0.79 | Dual NHAI + irrigation revenue base |

Zero promoter pledging across all four, the forced-sell risk is eliminated entirely.

For government-owned deep-value names, see our dedicated guide on high book value government stocks.

Not all ten names carry equal confidence. Here is how to think about position sizing:

This list is the starting point, not the finish line. Before committing capital to any name here:

Read the last two annual reports, specifically the Notes to Accounts, Related Party Transactions, and Contingent Liabilities schedule. This is where the risks that screeners cannot see are disclosed.

Check the cash flow statement. Net profit versus operating cash flow conversion is the most important data point not visible in any standard screener table.

Define your catalyst. Cheap without a re-rating event is just cheap. Name the specific development — NHAI payment normalisation, paper cycle recovery, contract renewal, that will close the valuation gap, and set a realistic timeframe for it.

For investors who want to combine individual stock picks with a disciplined passive core, our guide on ETF vs Index Fund Strategy in India covers how to blend active deep-value selection with index exposure to reduce stock-specific risk.

Research Disclaimer: This article is prepared for informational and educational purposes only. It does not constitute investment advice or a recommendation to buy or sell any security. All data is sourced from public disclosures and verified as of May 2026. Equity investments are subject to market risk. Readers are advised to consult a SEBI-registered investment advisor before making investment decisions.

Identifying genuine high book value low PE stocks in 2026 requires more than a simple filter pass. By focusing on the Double Discount, you secure a strategic margin of safety where market prices sit below both net worth and industry multiples. Remember, the most successful high book value low PE stocks are those with clean balance sheets and zero pledging. Stick to these pillars to build lasting wealth.

Related Reading from Lakshmishree:

No, a low price alone is not a green signal. While a market price below book value essentially translates into a discount on assets, you must first determine if those assets are productive or impaired. If a company owns old machinery that no longer works or has massive Goodwill on its books, the book value is effectively a ghost. You should only consider it a buy if the company also maintains a Positive Net Profit, which is to say the assets are still generating real cash.

The most common reason is the Liquidity and Trust Gap. Smaller companies often lack institutional interest, otherwise known as a lack of "smart money" participation. Furthermore, many of these firms carry hidden risks like Promoter Pledging, where the owners have pawned their shares for personal loans. If the debt is high and the volume is low, the stock stays cheap because the market doesn't trust the numbers. This results in a net stagnation that keeps your capital trapped for years, regardless of how cheap the paper price appears.

A low P/E can be a deceptive signal if the company’s earnings are "cyclical." In sectors like Steel or Paper, a company might show a P/E of 4 at the very top of a boom, which essentially translates into a warning that profits are about to fall. Savvy investors use the Neighborhood Rule by comparing the stock to the Industry PE. If the stock is cheap but its ROCE is declining, the market is pricing in a future disaster. Put a pin on this for a moment: a low P/E is only a bargain if the company’s internal profit engine is still running faster than the cost of its debt.

Debt is the ultimate Book Value Killer. If a company has one thousand crores in assets but owes eight hundred crores to the bank, your equity is only the small slice left over. In a crisis, the lenders have first claim on everything, effectively leaving you with zero protection. This is why we insist on a Debt to Equity Ratio below 1.0. It ensures that you, the shareholder, actually own the majority of the business. When the debt is low, the book value acts as a structural floor. When the debt is high, that floor is made of thin glass.

A company becomes one of these high book value low pe stocks by offering a Double Discount. This essentially translates into paying less than what the company’s physical assets are worth, while the business also generates profits faster than its competitors. This move is akin to buying a successful shop for less than the value of the building and equipment itself.

These stocks are resilient because they possess a structural floor. Since the price is below the value of real land and cash, buyers usually step in to stop a fall. Contrastingly enough, this only works if assets are tangible. If the worth is based on paper-only fluff, that floor is made of glass, effectively leaving you unprotected during a panic.