Imagine you lent your neighbour ₹10,000. He never paid it back. Your wallet is now empty, your EMI date is crawling near, and rent is knocking on the door.

The problem is not that you spent carelessly. You are in financial difficulty because someone else's problem became yours because of a bad loan.

That, in essence, is what happened to India's banks between 2008 and 2017. At a scale involving lakhs of crores. And the solution the government found to fix it is one of the most elegant financial manoeuvres any government has ever pulled off.

Related Reading from this Article: What is Non-Performing Assets in Banking.

Recapitalization is the process of injecting fresh capital into a weakened bank so it can function normally again.

Think of every bank standing on a two-legged stool:

| Leg | What It Is | How It Works |

| Equity | The bank's own permanent money | Does not carry interest, forms the safety shield |

| Debt | Borrowed money | Must be repaid with interest |

Together, they form the bank's capital structure. When bad loans erode the equity leg, the stool tips.

Recapitalization involves injecting fresh capital to rebuild that equity shield, allowing the bank to meet its obligations and satisfy its regulators.

Injecting capital directly inflates the accounting net worth. This shift is why we monitor; What is book value of a share to find genuine value.

Between 2008 and 2015, India's 21 Public Sector Banks, holding the savings of hundreds of millions of ordinary Indians, went on an aggressive lending spree.

Who got the loans:

The economy was growing. The optimism was genuine for the time being. The lending looked rational at the time.

Then the projects stalled.

Construction timelines blew past deadlines. Commodity prices fell. Power plants could not find buyers for the electricity they were supposed to generate. And the borrowers, many of them large, politically connected promoters, simply stopped repaying.

In banking, when a borrower stops repaying for more than ninety days, that loan is officially reclassified as a Non-Performing Asset, otherwise known as an NPA or bad loan.

From here the math gets deeply uncomfortable.

An NPA does not sit quietly on a bank's books. It actively destroys the bank's capital base. Every rupee of a bad loan forces the bank to provision, which means setting aside money from its own equity reserves to cover the expected loss.

| What Happens | The Effect |

| Borrower stops repaying | Loan becomes NPA |

| NPA classified | Bank must provision from equity |

| Provisioning increases | Equity shield erodes |

| Equity shield erodes | Capital adequacy falls |

| Capital adequacy falls | RBI activates PCA restrictions |

The worse the NPA pile grows, the faster the equity shield erodes, resulting in a net deterioration that compounds with every passing quarter.

By 2017, the Reserve Bank of India's Asset Quality Review forced banks to honestly recognise their bad loans for the first time. The results were alarming:

The stool had lost its equity leg.

A rescued balance sheet is only as good as the loans behind it. To verify if a bank's recovery is real, audit: What is Non-performing asset and Net NPA ratios.

When a bank's capital falls below the minimum threshold required under Basel III norms, the RBI does not simply send a warning letter. It activates the Prompt Corrective Action framework, otherwise known as PCA.

Under PCA, a bank is placed in effective regulatory detention:

And here is the paradox that makes this crisis stranger than it sounds.

The banks were not actually empty of cash. Following demonetisation in 2016, the banking system was overflowing with depositor liquidity. The RBI estimated somewhere between ₹2.8 lakh crore and ₹4.3 lakh crore in additional deposits had flooded in as people exchanged their old currency notes.

The money was there. But because the banks were trapped in PCA restrictions, and contrastingly enough were terrified of creating more NPAs, they refused to lend it out. They locked the excess cash away in safe government securities instead.

Economists gave this a name: Lazy Banking.

Much like a river dammed at both ends, the water was there but going nowhere. Without lending, businesses could not invest. Without investment, growth slowed. The NPA crisis was not just a banking problem. It was paving the way for a broader economic paralysis.

The government had to act. Fast.

The obvious fix was simple. The government injects fresh equity into the banks, rebuilds their capital base, lifts the PCA restrictions, and restores lending.

One colossal problem.

The government's own treasury was under severe pressure. India's fiscal deficit, which is the gap between what the government earns and what it spends, was already stretched close to its limits.

If the government simply borrowed ₹2 lakh crore and handed it directly to PSU banks:

| Consequence | Impact |

| Money appears in fiscal deficit | Breaches deficit targets |

| Deficit breach triggers | Sovereign credit rating downgrade |

| Rating downgrade risks | Currency destabilisation |

The problem was real. The solution was obvious. And the means to execute the obvious solution simply did not exist.

So the government did something far more elegant. It engineered a transaction where the cash never actually left the banking system at all.

Recap bonds, also written as recapitalization bonds, are special government securities issued not to the general public, but directly to the PSU banks themselves, with the explicit purpose of rebuilding those banks' equity capital.

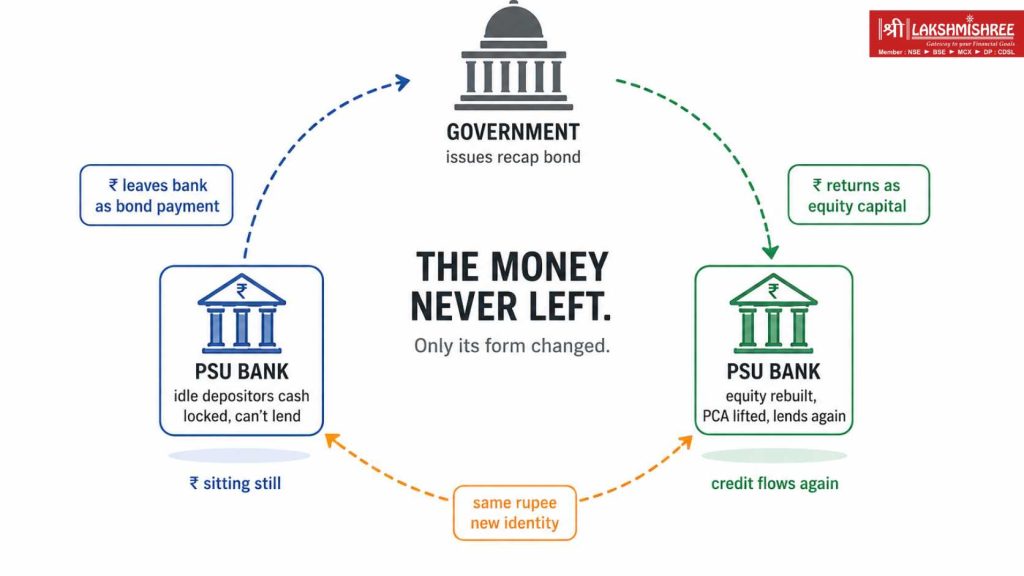

Here is the mechanism. Follow it carefully, because once you see it, you cannot unsee it.

Step 1: Government Creates the Bond

The government creates a bond, a sovereign certificate carrying the full guarantee of the Government of India, promising regular interest payments over its lifetime. It offers this bond to a PSU bank.

Step 2: Bank Buys the Bond

The bank, sitting on its mountain of idle depositor cash that it cannot lend out anyway, buys the bond. Cash flows from the bank to the government.

Step 3: Government Returns the Cash as Equity

The government is now holding the cash it just raised. It turns around immediately and injects that exact same cash back into the bank, not as a deposit return, but as equity capital, effectively purchasing new shares in the bank.

The concept: The money moved in a circle, but the identity it carried changed on the way around. That legal transformation, from liability to equity, is what made the whole operation possible.

The shield was rebuilt. The NPA hole was patched. The PCA prison doors opened. And the government had done the entire operation without a single rupee leaving the fiscal budget as direct expenditure.

In corporate finance, the term "recapitalization" also appears in two other forms; Leveraged Recapitalization and Dividend Recapitalization. These are private sector instruments used to restructure company ownership, not to rescue banks. This article covers government bank recapitalization specifically. The corporate variants are explained briefly at the end for completeness.

If the government is injecting lakhs of crores into banks, why does it not show up in the fiscal deficit?

The answer is in the accounting classification.

| Type of Transaction | Hits Fiscal Deficit? | Example |

| Revenue expenditure | Yes | Salaries, subsidies, goods |

| Capital transaction | No | Swapping one financial asset for another |

Recap bonds are classified as a capital transaction, an exchange of one financial asset for another, rather than a revenue expenditure. The government is not spending money on goods, salaries, or subsidies. It is swapping a paper instrument for equity shares.

Under IMF accounting conventions, which India follows, this transaction is excluded from the fiscal deficit calculation. It is, however, counted in the government's internal debt, because the bonds carry interest obligations and those annual interest payments do flow through the budget each year.

The annual interest burden on the original recap bonds was estimated at approximately ₹9,000 crore per year, which is significant but a far cry from what a direct ₹2.11 lakh crore fiscal injection would have cost.

The mechanism was not new. It was a proven financial tool that the government drastically scaled and refined over three decades to meet a national crisis.

| Year | Event | Significance |

| 1993–1994 | India first used recapitalization bonds during the banking crisis following the 1991 liberalisation reforms | Established the legal and accounting framework for all later interventions |

| October 24, 2017 | Finance Minister Arun Jaitley announced the unprecedented ₹2.11 lakh crore recap package | The RBI Governor called it a "monumental step forward in safeguarding the country's economic future" |

| 2020 | Government introduced Zero-Coupon Recapitalization Bonds | A cleaner, evolved version of the instrument — explained below |

Standard recap bonds carry annual interest obligations of roughly ₹9,000 crore per year flowing through the budget. The 2020 zero-coupon variant removed even this ongoing cost.

| Standard Recap Bond | Zero-Coupon Recap Bond | |

| Annual Interest Paid | Yes, ~₹9,000 Cr/year | No |

| Budget Impact (Annual) | Interest flows through each year | Zero annual cash drain |

| Loop Mechanism | Same | Same |

| Equity Rebuild | Yes | Yes |

The government still issues the bond. The bank still buys it. The equity loop still closes. But the annual fiscal burden disappears entirely. That is not a minor refinement. That is a structurally cleaner version of the instrument that removes even the ongoing cost of the bailout.

Punjab National Bank is one of India's biggest government banks and was one of the hardest hit by the bad loan crisis. Lets look at what happened;

Where PNB stood at its worst:

| Year | Amount Received |

| 2017–2018 | ₹11,678 crore |

| 2018–2019 | ₹25,839 crore (largest single-year infusion in its history) |

| 2019–2020 | ₹17,757 crore |

| Total | Over ₹55,000 crore |

| Metric | At Crisis Peak | By 2022–2023 |

| Gross NPA Ratio | Above 18% | Under 9% |

| Net Profit | Years of losses | ₹3,457 crore profit |

| PCA Status | Under restriction | Lifted, fully operational |

The capital injection did not fix PNB's problems overnight. But it gave the bank the capital runway to survive long enough to fix those problems itself. Similar to medicine that does not cure the disease instantly. It kept the patient stable long enough for the patient to heal themselves.

That is what recapitalization of public sector banks looks like when it works.

The recap bond story did not end in 2020. Here is what happened next.

| Indicator | 2017 (Crisis Peak) | 2025 (Current) |

| Gross NPA Ratio of PSU Banks | 14.6% | ~2.1–2.5% |

| Banks Under PCA | Multiple | Most released |

| PSU Bank Credit Growth | Stalled | Double-digit recovery (SBI, BoB) |

| Lazy Banking Status | River dammed at both ends | Credit flowing again |

India's gross NPA ratio falling from above 14% to approximately 2.1 -- 2.5% by 2025 is one of the sharpest banking sector recoveries in emerging market history.

The dammed river finally flowed. Businesses could borrow again. Growth resumed. The Lazy Banking era ended because recap bonds gave PSU Banks the capital base they needed to start lending without existential fear.

The banking turnaround makes top government banks in India highly attractive. You can see the effects in our audit of the most profitable PSU bank stocks today.

Go back to the neighbour who never repaid your ₹10,000. Now imagine it was not one neighbour. There were thousands of them. And the wallet that was emptied belonged not to you personally, but to a bank holding the savings of crores of ordinary Indians.

The government faced that situation in 2017 with no money to directly fix it and no room to borrow more. Going to a moneylender, meaning direct fiscal borrowing, would have blown the deficit, triggered a credit downgrade, and destabilised the currency.

So instead the government found the money that was already sitting inside the banking system itself, sent it around a carefully engineered loop, and returned it wearing an entirely different legal identity. Idle depositor liquidity arrived back as permanent equity capital, rebuilding the shield, lifting the PCA restrictions, and restarting the credit engine of an economy that had been holding its breath.

PNB went from regulatory detention to profitability. The system's NPA ratio fell from 14.6% to approximately 2.1%. A dammed river started flowing again. And a brilliantly structured piece of paper did all of it without a single rupee showing up in the fiscal deficit as direct expenditure.

The honest answer is: yes, eventually, but not all at once. As recap bonds are treated as a capital transaction, the initial massive injection (like the ₹2.11 lakh crore in 2017) does not hit the government's fiscal deficit immediately. However, the government must pay annual interest on these bonds. That interest is paid out of the annual Union Budget, which is funded by taxpayer money. You are not paying for the massive principal upfront; you are paying the EMI on the bailout over the next 10 to 15 years.

When the government injects recap bonds into a bank, it receives new equity shares in return. This instantly dilutes the ownership percentage of existing retail shareholders. However, without this capital, the bank would remain paralyzed under PCA (Prompt Corrective Action) or face collapse. Historically, while the immediate reaction might be concern over dilution, the long-term stock price usually recovers (as seen with PNB) because the bank is finally permitted to clean its balance sheet, issue new loans, and return to profitability

A normal government bond is sold in the open market to raise cash for building roads or paying salaries. A Recapitalization Bond is a closed-loop instrument. It is issued only to specific struggling PSU banks. It is generally non-tradable, meaning the bank cannot sell it to the public. Its sole purpose is an accounting maneuver: to take the bank's idle cash liabilities and transform them into Tier-1 equity capital so the bank satisfies RBI regulations.

Yes. Recapitalization is the ultimate proof of the sovereign guarantee.

When the government engineered this massive financial loop, it was explicitly to prevent a systemic collapse of banks holding public savings. By replacing the eroded capital with sovereign-backed bonds, the government proved it will structurally intervene to protect Public Sector Banks. The NPA crisis was the closest the Indian banking system came to the edge, and the recap bonds were the safety net that caught them.

As printing money to cover bad loans triggers inflation, it effectively makes every citizen poorer to pay for the mistakes of a few corporate defaulters.

The recap bond was an elegant solution precisely because it did not create new money. It simply repurposed the massive pool of idle cash already sitting inside the banking system (largely driven by the 2016 demonetization). It fixed the banks' balance sheets without artificially inflating the national money supply.