You open your mutual fund app. You see the Flexi Cap Fund among many categories. Some you know very well like Large Cap, small cap etc. Naturally you think, what does flexi cap even mean? Is it different from large-cap? Mid-cap? what should i know before I invest?”

Here’s the simple answer:

A flexi cap fund is a mutual fund that invests in companies of ALL sizes-large, medium, and small without any fixed restrictions. The fund manager has complete freedom to decide how much to invest in each category based on where they see the best opportunities.

Think of this guide as your Master key to unlock how these flexible funds work and the tax benefits they offer in 2026. We’ll break down the difference between flexi cap and large cap, mid cap, or small cap funds, highlighting the benefits and drawbacks.

A flexi cap fund is an equity mutual fund that can invest across large-cap, mid-cap, and small-cap stocks without any minimum allocation requirements. Fund managers have complete freedom to shift money between company sizes based on valuations, market conditions, and growth opportunities.

An open-ended dynamic equity scheme investing across large cap, mid cap, small cap stocks. The only rule: Minimum 65% of total assets must be in equity and equity-related instruments.

It highlights that while the fund is "open-ended" and "dynamic" (meaning it can change size and shape anytime), it must always keep at least 65% of its money in the stock market to qualify for equity tax benefits.

What this means in simply:

This is what makes flexi cap different from every other equity fund category.

Flexi means the manager has the freedom to move money wherever he analyzes the growth is. Cap refers to the size of the company. It’s a strategy that adapts to the market, using stable giants for safety and smaller, fast-growing firms for profit.

The fund that can be changed easily, i.e. it can FLEX, among different types of stocks:

No fixed percentages. Changes based on opportunities.

Market capitalization (or “market cap”) is the total value of a company’s shares, calculated by multiplying the current share price by the total number of outstanding shares.

Market capitalization = Total value of a company’s shares

Formula: Share Price × Total Number of Shares

Example: Reliance Industries:

SEBI classifies companies into three categories:

| Category | Ranking by Market Cap | Examples (March 2026) |

|---|---|---|

| Large Cap | Top 100 companies | Reliance, TCS, HDFC Bank, Infosys |

| Mid Cap | Rank 101 to 250 | Dixon, Persistent Systems, Coforge |

| Small Cap | Rank 251 and below | Rail Vikas Nigam, Happiest Minds |

A flexi cap fund operates through continuous market analysis, portfolio rebalancing, and allocation shifts across market caps. The fund manager actively monitors opportunities and adjusts holdings to capture the best risk-reward scenarios.

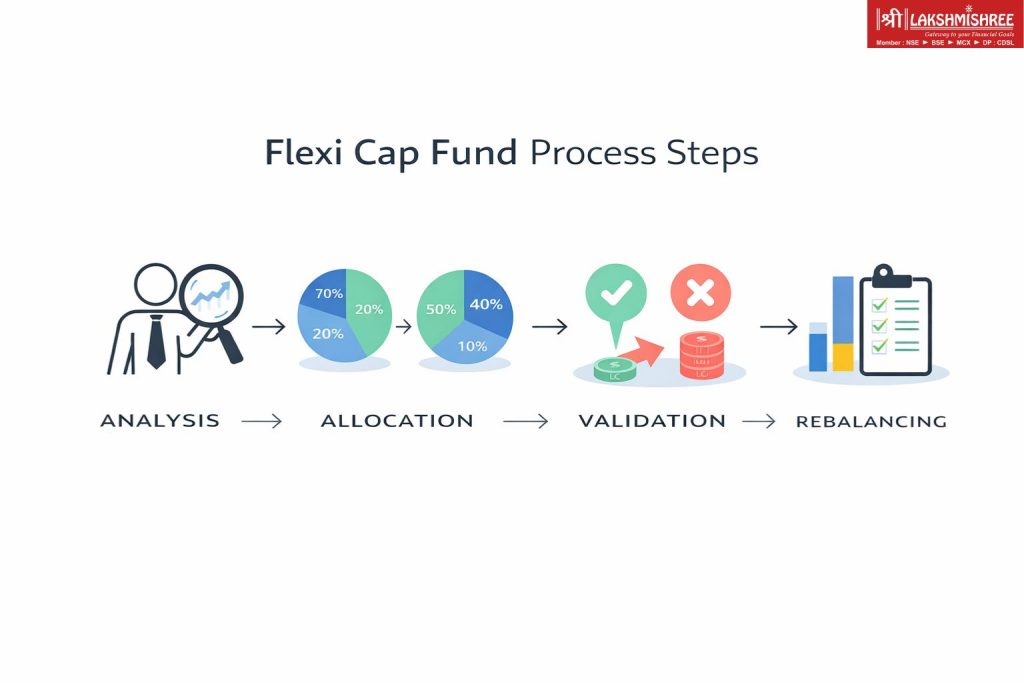

For example, in March 2024, the market was shifting. Here is exactly how a Flexi Cap manager moves your money from expensive stocks into better deals and what happens to your returns when they do.

Let’s follow a typical flexi cap fund’s journey:

This is the investigative phase where the fund manager evaluates the "fair value" of different market segments. The fund manager evaluates valuation metrics (P/E ratios, growth rates, earnings quality) across large-cap, mid-cap, and small-cap stocks to identify which segment offers the best risk-adjusted opportunities. The goal is to identify if a sector is Overvalued (trading above its worth) or Undervalued (selling at a discount).

In March 2024, the market presented a clear valuation gap that required a tactical decision:

Fund manager takes a decision: "Large caps are currently overpriced and offer a limited room to grow. I will reduce our exposure here and turn toward the better value found in Mid Caps.”

Based on the analysis, the fund manager sells overvalued holdings and buys undervalued ones, gradually shifting the portfolio’s market cap mix.

| Market Segment | Old Allocation (Feb 2024) | New Allocation (Mar 2024) | Action Taken |

| Large Cap | 70% | 50% | Reduced by 20% (Profit Booking) |

| Mid Cap | 20% | 40% | Increased by 20% (Value Buying) |

| Small Cap | 10% | 10% | Unchanged (Selective Holding) |

The manager successfully unlocked 20% of the portfolio from stagnant, overpriced Large caps and reinvested it into the high-potential mid-sized companies identified in Step 1.

This happens over days/weeks through buying and selling stocks.

In this stage, If the manager’s strategy is correct, the fund achieves extra profit compared to a basic, unmanaged fund. However, there is always a risk: if the market moves in the opposite direction of the manager's plan, the fund will underperform, meaning it earns less than a simple, fixed-category index.

Scenario A - If Fund Manager Was Right about his decision:

In this case, the manager’s timing was perfect. The market rewarded the value in mid-sized firms while the giants slowed down.

Fund manager’s flexibility captured an extra 5.5% returns.

Scenario B - If Fund Manager decision was Wrong (it is possible):

Markets can be unpredictable. Sometimes, expensive stocks keep getting more expensive, while the better deals take longer to grow.

Fund underperforms. Risk of active management.

Unlike static investment that you buy and forget, fund manager's strategy involves constant, small adjustments to protect your money and find new growth for you. This professional oversight is exactly what you pay for through the Expense Ratio (the annual management fee).

How your Fund Managers find growth for you :

This active management is what you’re paying the expense ratio for.

Flexi cap funds differ from other equity fund categories in their allocation flexibility. While large cap, mid cap, and multi cap funds have SEBI-mandated restrictions, flexi cap funds have complete freedom except for the 65% minimum equity requirement.

This is where most confusion happens. Let’s clear it up:

A Large Cap Fund is built for safety, focusing only on India’s top 100 giant companies. In contrast, a Flexi Cap Fund is made for speed; it has the freedom to shop across the entire market, grabbing profit wherever it finds it. the profit could be from a big, famous brand or a fast-growing medium-sized star.

Here is a table to understand the difference between large-cap fund and flexi cap fund:

| Aspect | Flexi Cap Fund | Large Cap Fund |

|---|---|---|

| Investment scope | All company sizes | Only top 100 companies |

| SEBI Requirement | 65% equity (no cap restriction) | 80% in large cap stocks |

| Risk | Moderate to High | Moderate |

| Returns Potential | Higher (can capture mid/small cap rallies) | Moderate (limited to large caps) |

| Volatility | Higher | Lower |

| Best For | Growth + some stability | Stability + steady growth |

When flexi cap wins: Mid/small caps are rallying (2024-25 example: mid caps +42% vs large caps +18%)

When large cap wins: Market uncertainty, corrections (large caps fall less)

A Mid Cap Fund targets high growth by focusing only on medium-sized companies. they are the "next generation" of market leaders. In contrast, a Flexi Cap Fund focuses on balance; it can switch between these fast-growing stars and stable giants to give you a smoother ride when the market gets uneven.

Mid cap vs flexi cap fund comparison table

| Aspect | Flexi Cap Fund | Mid Cap Fund |

|---|---|---|

| Investment Focus | Flexible across all caps | 65%+ in mid cap stocks (rank 101-250) |

| Downside Protection | Can shift to large caps during crash | Stuck in mid caps |

| Upside Potential | Captures mid cap rallies partially | 100% exposure to mid cap gains |

| Volatility | Moderate-High | Very High |

| Best For | Balanced growth seekers | Aggressive investors |

When flexi cap wins: Market corrections (shifts to large caps for safety)

When mid cap wins: Strong mid cap rally (100% exposure in mid cap vs flexi cap’s 30-40%)

A Multi Cap Fund is built for forced diversification, as SEBI rules mandate they must always hold at least 25% each in Large, Mid, and Small companies. In contrast, a Flexi Cap Fund is built for total freedom; it allows the manager to move 100% of your money into safer, large companies if they sense a market crash is coming.

This is the most confusing comparison because they sound similar, lets understand this with a table:

| Aspect | Flexi Cap Fund | Multi Cap Fund |

|---|---|---|

| SEBI Mandate | 65% equity, no cap restriction | 75% equity + 25% minimum EACH in large/mid/small |

| Flexibility | Complete freedom | Restricted by 25-25-25 rule |

| Manager Decision | Can go 100% large cap if needed | Cannot go below 25% in any category |

| Risk Management | Dynamic (can reduce risk by shifting to large caps) | Forced diversification |

| Best For | Active management believers | Want automatic diversification |

Key difference in one example:

Market scenario: Small caps crash -30%, large caps stable.

Flexi cap manager: Exits small caps completely, moves to large caps (protects capital)

Multi cap manager: Stuck with 25% in small caps (mandatory SEBI rule), suffers loss

This flexibility is why flexi cap funds gained ₹2.3 lakh Crore AUM since 2020.

Wondering if you should invest all at once or bit-by-bit? See our analysis on

SIP vs. Lump Sum Investment

to find the best strategy for current market conditions.

Choosing a Flexi Cap Fund is like hiring a professional navigator for your investment journey. Instead of you having to guess when to move your money between big, stable companies and fast-growing small ones, a seasoned fund manager does this for you, every single day. This "always-ON analysis" approach simplifies your life by packing professional market timing, automatic diversification, and built-in crash protection into a single, tax-efficient investment.

Here are the four standout benefits that make this category a favorite for 2026:

This is the process of automatically buying low and selling high within the fund. Instead of the investor guessing when to move money between big and small companies, the fund manager uses real-time data to "rotate" the capital into the most promising sectors

Without flexi cap:

With flexi cap:

Example:

2022-2023: Small caps expensive → Flexi cap managers reduced small cap from 15% to 5%

2024: Mid caps attractive → Increased mid cap from 25% to 45%

You, as an investor: Did nothing. The Fund Manager did it automatically.

Instead of buying three separate, specialized funds (Large, Mid, and Small Cap) to build your equity portfolio, a Flexi Cap fund acts as your Master Fund. It holds all these categories under one umbrella, providing instant, broad-market diversification without the need to manage multiple schemes.

Instead of:

You can:

Simplifies:

Who benefits most: Beginners, busy professionals, NRIs ( those who can’t actively manage)

A Flexi Cap fund has the freedom to follow the money growth sectors. As Markets move in cycles. Big, mid-sized, and small companies each take turns leading the way. Instead of staying in one fixed way or a slow lane, the manager moves your investment into whichever category is currently growing the fastest.

Market cycles rotate:

Flexi cap captures each phase by shifting allocations.

Downside Protection Through Flexibility means that the fund’s ability to reduce it's risk when the market gets scary or unpridictable. When prices crash, small companies usually fall the hardest. A Flexi Cap manager can quickly move your money into Safe Haven giants (Large Caps) to protect your capital from deep losses.

During market crashes:

March 2020 (COVID crash):

Flexi cap fund response:

Recovery:

This dynamic risk management is FlexiCap’s biggest advantage.

While the freedom of a Flexi Cap fund is its greatest strength, that same freedom creates specific trade-offs. Since you are giving the steering wheel of your investment to a professional, your success depends on their skills and the cost of their expert management. Understanding these trade-offs is key to making sure this all-weather plan really fits your long-term goals.

Your returns are directly tied to the individual making the decisions. Unlike an "Index Fund" that follows a fixed list, a Flexi Cap fund’s success is 100% dependent on the manager’s ability to predict market shifts correctly

Same flexi cap category, different results (2024-25) managed by a different Manager:

Risk: If fund manager makes poor decisions, your returns suffer.

Mitigation: Choose flexi cap funds with experienced managers, proven 5+ year track records.

Active management requires a team of researchers and analysts, which costs money. This fee, known as the Expense Ratio, is deducted from your returns annually. Over a decade, even a small percentage difference can cost you lakhs in potential wealth.

Active management costs money:

Comparison:

Impact on ₹10 lakh over 10 years:

Is it worth it? Only if fund consistently beats benchmark by more than expense ratio difference.

Unlike a Multi Cap fund (which must hold 25% in small companies), a Flexi Cap manager can decide to hold 0% in small companies if they feel like it. You lose direct control over what size companies you want to own.

With multi cap fund: You KNOW you have 25% each in large/mid/small (forced diversification)

With flexi cap: Today 70% large cap, tomorrow 40% large cap. You don’t control it.

Risk scenario:

You invested in a flexi cap because you wanted mid-cap exposure (mid-caps looked attractive).

But: Fund manager stays 80% in large caps (conservative approach).

Result: You missed the mid cap rally you wanted.

Solution: Check fund’s historical allocation patterns before investing. If fund is consistently 70%+ large cap, it’s essentially a large cap fund with flexi cap label.

A Flexi Cap fund is built to smooth the ride of the uneven stock market, not to be the fastest car on the track. Because they always keep some money in (safe) large companies, they will rarely be the top performer during a massive, all-out boom in small or mid-sized stocks.

Bull market (everything rising):

You might feel: “I should’ve just bought mid cap fund!”

But remember: In the next correction, that mid-cap fund might fall -40%, flexi cap will fall -22%.

Flexi cap smooths the journey (moderate gains, moderate falls). Not for maximum returns.

For new investors, flexi cap funds eliminate the guesswork of choosing between big or small stocks by providing a ready-made slice of the entire market. It is the fastest way to start building wealth without needing to be a professional.

Why flexi cap is perfect:

How much: 70-80% of equity allocation

Recommended funds: HDFC Flexi Cap, Parag Parikh Flexi Cap (proven track records)

Think of this as a self-correcting investment plan that adjusts itself as the economy changes. Instead of you spending hours researching what to buy next, a professional manager acts as your full-time market navigator, moving your money into the safest and most profitable sectors while you focus on your career.

Why flexi cap works:

How much: 50-60% of equity allocation.

Strategy: SIP in flexi cap + some index funds for passive exposure

The flexi cap continuously rotates capital between industry giants and emerging stars, ensuring your portfolio remains aligned with the market's highest-momentum sectors throughout every economic cycle.

Why flexi cap fits:

How much: 40-50% of equity allocation

Additional: Can add sectoral funds (10-15%), international equity (5-10%) for further diversification

The flexi cap anchors your money in India’s most reliable, Blue Chip giants, only a small amount in the high-speed growth stocks when the market is stable. It’s the ultimate way to participate in the stock market without losing sleep over sudden crashes.

Profile: Want equity returns but lower volatility than pure mid/small cap

Why flexi cap suits:

How much: 60-70% of equity allocation

Choose: Conservative flexi caps (HDFC, Kotak—70%+ large cap bias)

If you are sure that you have understood what is flexi cap funds and fall into one of these profiles, your next step is to compare actual performance or take action. We have curated a list of the

Best Flexi Cap Mutual Funds in 2026

based on rolling returns and manager expertise.

Picking a Flexi Cap Fund is like finding a skilled driver for your money. Instead of just chasing last year's highest profits, look for a fund that grows steadily and matches your risk level. By checking a few simple facts like the manager's experience and the fees they charge, you can pick a fund built to grow your wealth safely over time.

Instead of being blinded by a single year of surges, which can be regarded as lucky, 3 year consistency focuses on Repeated Success. It proves the fund manager follows a disciplined, repeatable process rather than just happening to be in the right place at the right time.

Don’t just see: “Fund gave 28% last year!”

Ask: Did it give consistent 18-22% over 3-5 years?

Red flag: 35% one year, 5% next year, 28% third year (inconsistent)

Green flag: 19%, 22%, 20% over 3 years (consistent)

Why: Consistency means fund manager has a proven strategy, not just luck.

Look past the name of the fund and see how the manager actually spent the money over the past two years. This reveals the real personality of the investment. You will find out if the fund prefers to stay safe with giant companies or hunts for big wins with smaller ones. Checking this helps you choose a fund that fits your own level of comfort.

Check last 8 quarterly reports. See pattern:

Fund A:

Fund B:

Choose based on YOUR risk appetite:

This is the Maintenance Cost of your investment just like a yearly membership fee you pay to the fund manager for managing your money. This fee is automatically taken out of your profits every single day. Even a small difference in this fee can grow into a massive amount of money over ten or twenty years.

Direct plan expense ratios:

WAIT: Always choose DIRECT plans (not Regular). Same fund, 0.5-1% lower expense.

You want to make sure the same Manager has been in charge for at least three years. If the person who made the fund successful leaves and a new one arrives, the new person might have a completely different way of doing things.

Stability matters:

Good: Same manager for 5+ years (proven strategy, consistent)

Caution: Manager changed 6 months ago (new strategy, unproven in this fund)

Why: Past performance is under OLD manager. New manager may have different style.

AUM is the total amount of money people have given the fund to manage. Think of it like the size of a ship. If the ship is too small, it might sink in a storm. If it is too big, it is harder to turn and move quickly tofind new treasures. You want a fund that is just the right size to be both safe and fast.

| The Pot Size | What it Means | The Level of Safety |

| Tiny (< ₹500 Crore) | The Danger Zone. | These funds are too small. They might struggle to buy and sell stocks easily or could even close down if they don't grow. |

| The Sweet Spot (₹2,000 to ₹50,000 Crore) | The High Performer. | This is the perfect size. The fund is big enough to be stable but small enough to move quickly and catch fast-growing companies. |

| The Giant (> ₹80,000 Crore) | The Slow Mover. | These funds are so heavy that it is hard for the manager to buy enough small, high-growth stocks to make a real difference to your profits. |

Exception: Parag Parikh (₹1.34 lakh Cr) works because of an international diversification strategy.

Let’s look at a typical flexi cap fund’s actual holdings (simplified example):

Total AUM: ₹25,000 Crores

Market Cap Allocation:

Top 10 Holdings:

| Stock | Market Cap | Allocation |

|---|---|---|

| HDFC Bank | Large | 7.2% |

| Reliance Industries | Large | 6.5% |

| ICICI Bank | Large | 5.8% |

| Infosys | Large | 5.2% |

| Axis Bank | Large | 4.1% |

| Dixon Technologies | Mid | 3.2% |

| Persistent Systems | Mid | 2.8% |

| Coforge | Mid | 2.5% |

| Rail Vikas Nigam | Small | 1.9% |

| Happiest Minds | Small | 1.6% |

Total Top 10: 40.8% of portfolio

Remaining 59.2%: Spread across 35-40 other stocks

What you notice:

This balance between large cap stability + mid/small cap growth opportunities is what defines flexi cap.

Since Flexi Cap funds keep at least 65% of their money in the stock market, they are taxed as Equity Funds. This is great news for your wallet because the government gives you a special tax break if you hold your investment for more than a year. By understanding these simple rules, you can keep more of your hard-earned profits and grow your wealth faster.

Equity taxation applies:

Tax: 20%

Example:

Tax: 12.5% on gains above ₹1.25 lakh exemption

Example:

Tip: ALWAYS hold flexi cap funds for 12+ months minimum to get LTCG benefit + ₹1.25L exemption.

Now that you understand what is a flexi cap fund, don't pick one at random. Review our data-backed rankings of the

Best Flexi Cap Mutual Funds in 2026

to see which schemes are leading the market this year.

Understanding what is flexi cap fund is the first step toward building a resilient, "all-weather" equity portfolio. By removing the rigid boundaries of company size, these funds allow expert managers to chase growth wherever it appears. whether in established giants or emerging mid-cap leaders. While they carry the inherent risks of active management and equity volatility, their ability to adapt to changing market cycles makes them an ideal core holding for both beginners and seasoned investors.

As you plan your financial journey, remember that the true strength of a flexi cap fund lies in its agility. It simplifies your investment process by providing a single-point solution for multi-cap exposure, effectively automating your diversification. If you are looking for a strategy that balances stability with upside potential, now is the time to evaluate what is flexi cap fund's role in your specific wealth-creation plan. Start small with a SIP, stay invested for the long term, and let professional flexibility drive your portfolio's growth.

A flexi cap fund has no fixed limits on company size (large, mid, or small). A multi-cap fund is legally required by SEBI to maintain at least 25% in each category at all times, offering less manager flexibility.

Yes. For those learning what is a flexi cap fund, it is considered a safer entry point into equity because it provides instant diversification across 40–60 companies of varying sizes, reducing the impact of a single stock's failure.

They are taxed as equity funds. Gains held over one year (LTCG) are tax-free up to ₹1.25 lakh and taxed at 12.5% thereafter. Gains held under one year (STCG) are taxed at a flat 20%.

Technically, yes. Unlike other categories, the fund manager has the mandate to move up to 100% into large-caps if they believe mid and small-caps are overvalued, providing excellent downside protection during market crashes.

Equity markets move in cycles; you should hold these funds for at least 5 to 7 years. This timeframe allows the fund manager to navigate different market phases and maximize the benefits of compounding.

Flexi cap funds are equity mutual funds subject to market risks and volatility. Returns mentioned are for illustration purposes based on historical data and do not guarantee future performance.

This content explains what is flexi cap fund for educational purposes. Not personalized investment advice. Assess your risk tolerance, investment goals, and time horizon before investing. Consult a SEBI-registered investment advisor for personalized guidance.

Mutual fund investments are subject to market risks. Read all scheme-related documents carefully before investing.