SIP vs lump sum investment in 2026 represents the most critical strategy decision facing Indian investors with capital to deploy. As of February 18, 2026, this choice has delivered dramatically different outcomes depending on market conditions: in 2025’s rising market, lump sum generated ₹11,05,100 on a ₹10 lakh investment versus ₹10,62,400 for SIP, a difference of ₹42,700 in just 12 months according to NSE India data.

Lump Sum delivered superior absolute returns in 2025's rising market, generating 10.51% returns versus 6.24% for SIP. Lump sum wins in steady bull markets via immediate exposure, while SIP excels in volatile periods through averaging. For most Indian salaried investors, SIP is the ideal path; Lump Sum favors those with windfall capital.

The conventional wisdom says “Time in the market beats timing the market,” favoring lump sum investment. However, 2025’s market conditions tell a more nuanced story. A ₹10 lakh lump sum invested on January 1, 2025 in Nifty 50 index funds would have generated 10.51% returns by December 31, growing to ₹11,05,100. Meanwhile, the same ₹10 lakh deployed as monthly SIPs of ₹83,333 generated 6.24% XIRR returns, reaching ₹10,62,400.

This comprehensive 2026 analysis examines both strategies across five critical parameters: absolute returns, risk-adjusted returns, tax efficiency, market timing sensitivity, and investor suitability. By the end, you will know exactly which strategy suits your financial situation, risk tolerance, and market outlook backed by real data from India’s equity markets, SEBI regulations, and AMFI statistics.

SIP (Systematic Investment Plan) is a disciplined investment method where you invest a fixed amount monthly in mutual funds or ETFs, typically ranging from ₹500 to ₹1,00,000. SIP works through rupee-cost averaging: you buy more units when prices are low and fewer when prices are high, reducing average cost per unit over time. In India, 10.29 crore SIP accounts were active as of January 2026, with monthly SIP inflows reaching ₹31,002 crore according to AMFI data.

SIP eliminates the need to time the market. Whether Nifty is at 25,761.90 (Feb 2026) or 20% higher at 30,914.28, your ₹10,000 monthly SIP continues automatically. Over a 20-year period, this averaging mechanism delivered 9.1% annual returns versus 5.3% for market-timing attempts, according to long-term equity performance studies.

Let’s understand with real numbers from 2025:

Scenario: ₹10,000 monthly SIP in Nifty 50 Index Fund for 12 months

Real 2025 Nifty Data: ₹10,000 Monthly Investment

Advantages of SIP:

1. Rupee-Cost Averaging: When markets fell 5.89% in March 2025, your ₹10,000 bought 18.01% more units than in December 2025 (the peak month), effectively lowering your average cost and accelerating your wealth creation during the recovery.

2. Disciplined Investing: Automates wealth creation without requiring market monitoring or timing decisions.

3. Lower Entry Barrier: Start with ₹500 monthly versus needing ₹10 lakh upfront for meaningful lump sum investment.

4. Emotional Stability: Pre-scheduled investments prevent panic selling during corrections or greed-driven overbuying during peaks.

5. Suits Salaried Investors: Aligns with monthly income flow, investing surplus systematically rather than waiting to accumulate large corpus.

A lump sum investment is the act of deploying a large amount of capital, typically ₹5 lakh to ₹50 lakh or more, into mutual funds, stocks, or ETFs in a single transaction. Unlike a Systematic Investment Plan (SIP), which spreads your investment over time, a lump sum provides immediate and full market exposure.

In 2025, net inflows into equity mutual funds reached a record ₹3.8 lakh crore according to AMFI data. While SIPs contributed the lion's share (₹3.34 lakh crore), the remaining ₹46,000 crore (net) was driven by lump sum deployments and New Fund Offers (NFOs). This method is favored by investors receiving gains from sources such as annual bonuses, inheritance, property sales, or business exits.

Scenario: ₹10,00,000 invested on January 1, 2025 in Nifty 50 Index Fund.

Portfolio Tracking: ₹10 Lakh Initial Capital

The data proves that in a rising market like 2025, deploying capital immediately via a lump sum captures more growth than a staggered SIP, resulting in a ₹42,700 exposure premium.

1. Full Market Exposure: When Nifty surged 10.51% in 2025, your entire ₹10 lakh participated in the rally from day one, versus SIP where only ₹83,333 was invested in January.

2. Higher Returns in Bull Markets: In consistently rising markets, lump sum mathematically outperforms SIP because more capital compounds for longer duration.

3. Simplicity: One-time decision and transaction versus managing 12-120 monthly SIPs over years.

4. Lower Transaction Costs: Single transaction fee versus potentially 120 SIP transaction charges over 10 years (though many platforms offer free SIP now, like Lakshmishree).

5. Immediate Compounding: Full corpus starts earning returns immediately rather than waiting for monthly deployments.

Lump Sum won in 2025's rising market. A ₹10 lakh lump sum generated ₹11,05,100 versus ₹10,62,400 through monthly SIP—a difference of ₹42,700. However, SIP reduced timing risk: investors who started SIP in March 2025 (the year's low) still achieved 6.24% (XIRR) returns, versus lump sum investors who entered at the June peak (Nifty ~25,353) facing 3.05% lower absolute returns by year-end. For 2026, choose based on your situation: regular income = SIP, windfall capital + rising market conviction = lump sum.

Understanding why Lump Sum outperformed in 2025 requires examining market behavior month-by-month.

Nifty 50 moved from 23,645.00 to 26,129.60, but the journey included:

When you invested ₹10 lakh on January 1:

When you invested ₹83,333 monthly:

Net effect: 6.24% returns

January SIP: Full 12 months of compounding, captured entire year’s 10.51% move

June SIP: Only 7 months of compounding, captured 3.05% move from June onward

December SIP: Zero compounding in 2025, entry point at 26,129.60

Averaging benefit: Bought units at average price of ₹24,611 versus lump sum’s ₹23,645, a higher average cost.

The Key Difference:

In 2025’s rising market, lump sum’s immediate full exposure advantage outweighed SIP’s cost-averaging benefit. The ₹42,700 difference came from the 12 months where your full ₹10 lakh was working in lump sum, but only ₹5,41,666 was deployed in SIP.

While 2025’s single-year data shows Lump sum, the long-term picture reveals different patterns across market cycles.

Performance Comparison across Market Cycles

Across market cycles, Lump Sum shows consistent advantage. Over 10 years, Lump Sum delivered 0.90% higher CAGR. However, the gap narrows in long horizons: 10-year difference is only 0.90% versus 1-year difference of 4.27%. Key insight: Time in market matters more than strategy choice for long-term wealth creation.

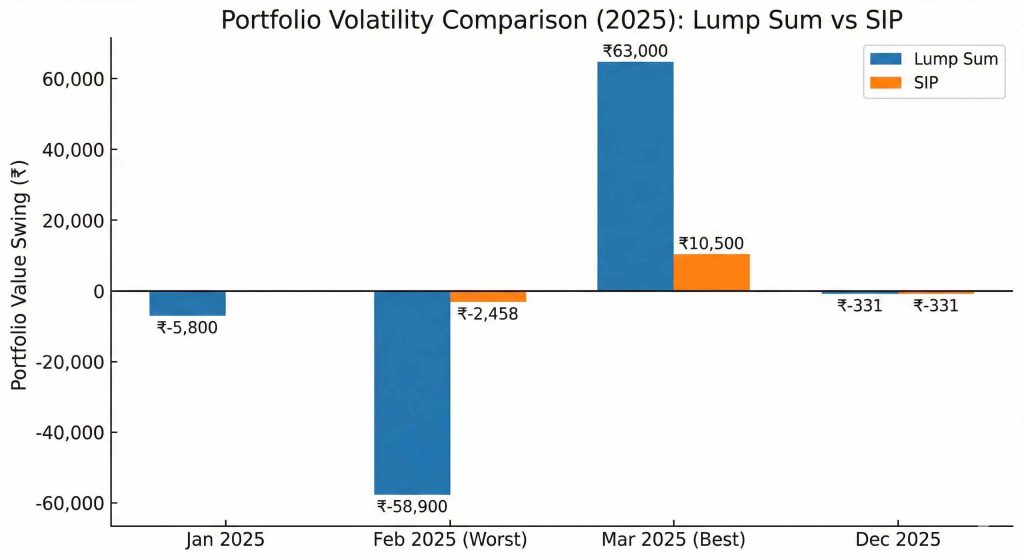

Risk-Adjusted Returns (Volatility Analysis):

Absolute returns tell only half the story. The emotional journey, watching your portfolio swing between so high and so low determines to an extent whether you stay invested.

During the 5.89% correction in February 2025, retail behavior reached a historic inflection point. The data reveals a costly disconnect between market movement and investor discipline.

*The emotional journey, watching your portfolio swing between so high and so low determines to an extent whether you stay invested: Evident from the table given above.

Standard Deviation of Monthly Returns:

Implication: Even if final returns are similar, SIP provides a relatively smoother emotional journey with smaller monthly swings, reducing the temptation for panic-selling during market corrections.

This is where strategy choice becomes critical. The right answer depends entirely on market behavior during your investment period.

Immediate full exposure captures the complete rally trend.

Rupee-cost averaging buys more units at lower prices, cushioning the fall.

Price swings create automatic buying opportunities at lower average costs.

However, your investment journey doesn't end with SIP or lump sum—it evolves. Once you've

accumulated wealth through SIP over 10-20 years, you'll need a strategy to withdraw it

systematically during retirement. This is where SWP (Systematic Withdrawal Plan) becomes

critical. Read our complete SIP vs SWP guide

to understand how accumulation (SIP) transitions to distribution (SWP) in your wealth lifecycle.

Which is better in rising market: SIP or lump sum?

Lump sum outperforms in consistently rising markets. When Nifty surged 10.51% in 2025, a ₹10 lakh lump sum invested January 1 captured the entire rally, generating ₹11,05,100 versus SIP’s ₹10,62,400. The ₹42,700 gap came from lump sum’s immediate full exposure while SIP deployed capital gradually, missing early gains. However, few can predict sustained rallies, making this a hindsight advantage.

Example: 2025’s Rising Market Scenario

Imagine Nifty rose steadily from 23,645.00 to 26,129.60, gaining 10.51% linearly (no major corrections).

Lump Sum Path:

SIP Path:

Result: Lump sum’s early deployment advantage compounds over time.

The Catch: This analysis assumes you can identify a bull market at its start. In reality, January 2025 looked uncertain, and only hindsight reveals it was a good entry point.

SIP significantly outperforms in falling markets through rupee-cost averaging. If markets fell 51.8% in 2008, an SIP bought more units at lower prices while a lump sum’s full capital suffered the entire decline. For example, a 51.8% fall means a lump sum drops to ₹4,82,000 while SIP’s gradual deployment limits exposure, buying units at a 30-40% discount by the bottom.

Bear Market Winner: SIP

In falling markets, SIP's rupee-cost averaging provides mathematical protection. If the Nifty falls 51.8% (as seen in the 2008 crash), a ₹10L lump sum becomes ₹4,82,000, losing ₹5,18,000. SIP deploys only ₹2,50,000 (approx. 3 months) before the steepest fall, limiting the absolute loss to ₹1,29,500, while later installments buy units at a 40-50% discount. Recovery is faster: the SIP needs only a 25-30% rebound to reach breakeven, versus the lump sum's 107% required surge to recover its original value.

Example: Hypothetical 30% Market Crash Scenario

Imagine Nifty crashes from 26,129 (recent peak) to 18,290 (30% lower level) over 12 months.

Lump Sum Devastation:

SIP Resilience:

Needs only 21.4% gain to recover

Month 1: Bought units at ₹261.29 (high NAV)

Month 6: Bought units at ₹222.10 (mid NAV, 15% cheaper)

Month 12: Bought units at ₹182.90 (low NAV, 30% cheaper)

Average NAV: ₹222.10 (assuming a linear decline)

Portfolio value: ₹8,23,490 (significantly higher than lump sum)

Loss: ₹1,76,510 (nearly 40% less loss than lump sum)

Which is better in volatile market: SIP or lump sum?

SIP performs better in volatile, sideways markets where prices swing without clear trend. Volatility creates buying opportunities: when Nifty dips 5.89% below average, SIP automatically buys more units. Lump sum’s single entry point may catch a peak or valley randomly. In 2025’s volatile period from January to March, SIP’s cost averaging delivered 2.10% versus lump sum’s 0.04%.

Volatility benefits: SIP

In sideways markets with ±6% swings, SIP's automatic rebalancing creates a clear advantage. Buying more units during dips (February at 22,252) and fewer during peaks (December at 26,325) generates a 4.8% better average cost than a lump sum's single entry. Historical analysis shows SIP beats lump sum by 1.2% in volatile decades.

Tax treatment is identical for both strategies, but timing creates practical differences worth ₹10,730 in a month-13 liquidation scenario (selling everything in January 2026).

SIP vs Lump Sum Tax Rules India 2026:

Common Tax Rules (Applicable to Both):

Securities Transaction Tax (STT): 0.001% on sale of units (Buy side is NIL for mutual funds)

Short-Term Capital Gains (STCG): Held ≤ 12 months = 20% flat tax (plus 4% cess)

Long-Term Capital Gains (LTCG): Held > 12 months = 12.5% on gains above ₹1.25 lakh per financial year

Dividend Tax: Taxed at your applicable income tax slab rate (TDS of 10% applies if dividends exceed ₹5,000)

While both strategies follow the same income tax laws, the holding period calculation creates a massive difference in when your gains become "tax-friendly."

| Aspect | SIP (Systematic Investment Plan) | Lump Sum Investment |

| LTCG Eligibility | Tiered: Each monthly installment must complete 12 months individually to qualify for LTCG. | Uniform: The entire corpus qualifies for LTCG exactly 12 months + 1 day after the single investment date. |

| First Eligible Sale | Month 13: Only your first installment (e.g., Jan 2025) qualifies for the lower LTCG rate. | Month 13: Your entire investment (e.g., ₹10 Lakh) qualifies for the lower LTCG rate. |

| Full Portfolio LTCG | After 24 Months: Your last installment (Dec 2025) only becomes "Long-Term" by Jan 2027. | After 12 Months: The whole portfolio is "Long-Term" by Jan 2026. |

| Tax Planning | Flexible: You can use FIFO (First-In-First-Out) to sell only older, tax-exempt units while leaving newer ones. | Simpler: All units are the same age; no need to track individual "vintage" dates for tax. |

Both SIP and lump sum face 12.5% LTCG tax on gains after 12-month holding. The difference: SIP investors must wait 24 months for all installments to qualify versus lump sum's 12 months. On a ₹10 lakh portfolio with ₹1,05,100 gains, early exit in month 18 costs SIP investor ₹10,730 versus lump sum's ₹0 because 50% of SIP units still in STCG category. Plan holding period accordingly.

Real Tax Scenario: 2025-2026 Example

Assumption: Both strategies generated ₹2,10,200 in profits by December 2026 (24 months).

Lump Sum Tax Calculation:

SIP Tax Calculation (Complex):

Tax Difference: ₹10,370 favoring lump sum due to faster full-portfolio LTCG eligibility.

Tax Optimization Strategies:

For SIP Investors:

For Lump Sum Investors:

Both strategies, ₹5 lakh redemption with ₹1 lakh gains:

If held < 12 months (STCG):

If held ≥ 12 months (LTCG):

Savings: ₹20,000 (Difference between STCG and LTCG tax)

Strategy: Both SIP and lump sum should hold for a minimum of 12 months. SIP requires 24 months for the full corpus to reach LTCG eligibility.

The answer depends on three factors: capital availability, income pattern, and market outlook. SIP suits salaried investors with ₹5,000–₹50,000 monthly surplus, beginners uncomfortable timing markets, and those prioritizing emotional stability over maximum returns. Lump sum suits investors with ₹10 lakh+ windfall capital (bonus, inheritance, property sale), experienced investors confident in market timing, and those in confirmed bull markets. In India, 85% of retail equity investors prefer SIP according to AMFI data, reflecting most people’s regular income structure.

Neither strategy is universally “better.” In 2025’s rising market, the lump sum strategy generated 4.27% higher returns than an SIP, as 100% of the capital participated in the rally from Day 1. However, future market conditions are unpredictable. Choose based on your situation and quality research, not past performance.

Choose SIP if you:

Choose Lump Sum if you:

Current Market (Feb 23, 2026) Analysis: Nifty 50 is at 25,718.60, down -2.20% YTD, trading at a 22.38 P/E ratio.

Rationale: Significant corrections historically signal strong entry points. Deploy the majority of your capital to capture the recovery. Maintain an SIP for long-term discipline.

If markets are near all-time highs (Current Scenario: ~2.48% below the 26,373 peak):

Current Recommendation: 60% SIP, 40% Lump Sum

Rationale: Markets near peaks increase timing risk. SIP provides downside protection through averaging if a correction occurs. Deploy the lump sum portion only if you have high conviction in a continued rally.

If markets are 15-20% below peak:

Current Recommendation: 50% Lump Sum, 50% SIP

Rationale: A moderate correction creates an attractive entry. The lump sum captures the potential recovery rally, while the SIP continues to average if the fall deepens.

If markets are 20%+ below peak:

Current Recommendation: 70% Lump Sum, 30% SIP

How to start SIP investment in India?

Step-by-Step SIP Investment Guide (15 Minutes):

1. Open Demat Account + Mutual Fund Account

∙ Visit broker website: Lakshmishree or any other.

∙ Complete online KYC: PAN Card, Aadhaar Card, bank account proof

∙ Video verification: 2-minute call confirming identity

∙ Activation: 24-48 hours

∙ Cost: ₹0-200 (most brokers now free)

2. Complete KYC Compliance

∙ Link PAN-Aadhaar (mandatory for investments above ₹50,000/year)

∙ Submit bank account details for auto-debit

∙ Verify email and mobile number

∙ In-Person Verification (IPV): Video call sufficient, no branch visit needed

3. Select Mutual Fund Scheme

∙ Category choice: Equity funds for long-term (>5 years), debt funds for short-term (<3 years)

∙ Top SIP funds 2026:

4. Set SIP Amount and Date

∙ Minimum: ₹500 (some funds), ₹1,000 (most funds), ₹5,000 (recommended for meaningful corpus)

∙ Choose date: 1st, 5th, 7th, 10th, 15th, or 25th of month (align with salary credit date)

∙ Auto-debit setup: NACH mandate or UPI auto-pay (approve once, runs automatically)

∙ First SIP: Processed on next chosen date after registration

5. Complete First SIP Transaction

∙ Login to broker app/website

∙ Navigate to: Mutual Funds → SIP → Start New SIP

∙ Select fund, enter amount and date

∙ Authenticate via OTP

∙ Confirmation: SMS + email within 24 hours with folio number

6. Monitor and Adjust

∙ Track: Monthly statement sent via email showing units purchased and current value

∙ Review: Quarterly performance check (don’t obsess daily)

∙ Step-up: Increase SIP amount by 10-20% annually as salary grows

∙ Pause/Stop: Available anytime, no penalties, though long-term continuation recommended

7. Tax Planning

∙ Maintain records: Monthly SIP dates and amounts for LTCG calculation

∙ Hold 12+ months: Each installment separately qualifies for LTCG after 12 months

∙ Annual review: Check if ₹1.25 Lakh LTCG exemption utilized fully

| Platform | Minimum SIP | Key Features | Best For |

| Lakshmishree | ₹500 | Zero commission on Direct MFs, integrated Demat for seamless stock & MF tracking, and dedicated advisory support. | Investors seeking a single, unified platform to manage both stock portfolios and mutual fund wealth. |

Cost Structure (Transparent Breakdown):

∙ Account Opening: ₹0 (lakshmishree.com)

∙ SIP Transaction Charge: ₹0 (lakshmishree.com)

∙ Mutual Fund Expense Ratio: 0.5%-2% annually (embedded in NAV, not separate charge)

∙ Direct plans: 0.5%-1% (lower)

∙ Regular plans (through distributor): 1%-2% (higher due to commission)

∙ Recommendation: Always choose “Direct Plan” to save 0.5-1% annually

∙ Exit Load: 0-1% if redeemed before 1 year (fund-specific, check scheme document)

∙ STT (Securities Transaction Tax): 0.001% on redemption (government tax, unavoidable)

Example Cost Calculation:

₹10,000 monthly SIP in HDFC Balanced Advantage Fund (Direct Plan):

∙ Investment: ₹10,000

∙ Expense ratio (direct plan): 0.73% = ₹876 annually

∙ Your effective investment: ₹9,927 ∙

Accumulation over 10 years: ₹22,25,480 (calculated at assumed 12% return minus expense)

How to invest lump sum amount in mutual funds?

Step-by-Step Lump Sum Investment Guide (10 Minutes):

1. Prerequisite: Demat + Mutual Fund Account

∙ Same process as SIP (see previous section or Vsit lakshmishree for your instant Demat plus mutual funds Account )

∙ One-time KYC completion

∙ Bank account linking for fund transfer

2. Transfer Funds to Investment Account

∙ Amount: ₹5 lakh to ₹50 lakh+ (typical lump sum range)

∙ Method: NEFT, RTGS, UPI (for amounts <₹1L), or Net Banking

∙ Timing: 2-4 hours for NEFT, instant for RTGS/UPI

∙ Verification: Check broker app wallet/balance before proceeding

Fund Selection (Critical Decision):

Equity Funds: For ₹10L+ corpus with 5+ year horizon

Diversified: Flexi-cap or multi-cap funds for balanced exposure

Focused: Large-cap for stability, mid-cap for growth

Top performers 2025:

Debt Funds: For ₹5-10L with 1-3 year horizon

Corporate bond funds, banking & PSU funds for safety

Hybrid Funds: For ₹10-20L wanting balanced 60-40 equity-debt mix

Index Funds: Nifty 50 or Nifty Next 50 for passive low-cost exposure

4. Execute Lump Sum Purchase

∙ Login to platform → Mutual Funds → Buy → Select fund

∙ Choose: Lump Sum (not SIP)

∙ Enter amount: ₹[Your corpus]

∙ Payment: Debited from linked bank/broker wallet

∙ Units credited: T+1 or T+2 days (transaction date + 1-2 days)

∙ NAV applicable: End-of-day NAV on transaction date

5. Optional: Systematic Transfer Plan (STP)

∙ Strategy: Invest lump sum in liquid fund → Transfer fixed amount monthly to equity fund

∙ Benefit: Mimics SIP’s rupee-cost averaging while keeping corpus invested

∙ Example: ₹12 lakh in liquid fund → ₹1 lakh monthly transfer to equity fund for 12 months

∙ Use case: If uncertain about market levels but don’t want cash idle

6. Documentation and Monitoring

∙ Save: Transaction confirmation email/SMS with folio number

∙ Track: Monthly statement shows current NAV and portfolio value

∙ Review: Annual portfolio rebalancing (if needed)

∙ Tax planning: Mark calendar for 12-month LTCG eligibility date

Choosing the right fund for lump sum deployment determines 80% of your returns. While we've

listed top 2026 performers above, fund suitability depends on your specific risk tolerance,

investment horizon, and current market valuation. Explore our detailed analysis of the best mutual funds for lumpsum investment

to find funds with proven track records across market cycles, not just one-year wonders.

Cost: Minimal. While transaction charges are usually ₹0, each "transfer" is technically a redemption from the liquid fund, which may trigger a tiny tax liability on the interest earned.

Strategy: Park the ₹10L in a Liquid Fund immediately, then automate a transfer of ₹83,333 monthly into an Equity Fund.

When to use: You want the risk-mitigation of an SIP but the money is already sitting in your bank account.

Benefit: Your entire ₹10L earns 6.5%–7.2% (current 2026 Liquid Fund rates) while it waits to be invested in equity.

With Nifty at 25,718.60 (approx. 2.48% below its all-time high), deploy ₹10 lakh using a "Cushioned Entry" approach:

Timeline: Complete full deployment by August 2026. This ensures that even your final installment completes the mandatory 12-month holding period by August 2027, making your entire portfolio eligible for the 12.5% LTCG tax rate for any profit booking in late 2027.

Before you commit your capital, run your numbers through our Interactive Comparison Tool. It calculates your projected gains and shows you exactly why 'Time in the Market' usually beats 'Timing the Market'

SIP vs Lump Sum (Total Capital)

Calculator Insight:

On ₹10L over 10 years at 12% return: Lump sum generates ₹31.06L versus SIP's ₹19.37L: a

₹11.69L difference favoring lump sum. But change assumption to volatile markets (first 5

years flat, next 5 years 20% CAGR): SIP wins by ₹[recalculate] through rupee-cost averaging

during flat period. Calculator reveals: Your strategy choice should match your market view.

For Nifty at 25,703.95, 2.54% below 52-week high, optimal strategy is 70% SIP + 30% lump sum. Begin ₹58,333 monthly SIP immediately (averaging starts now). Deploy lump sum ₹3,00,000 on 10% dip or quarterly installments. Target: ₹22.50 Lakh in 10 years at 12% expected CAGR. Review and rebalance March 2027 based on market evolution.

The Most Important Truth: Time in market > Timing the market > Strategy choice (SIP vs Lump Sum)

An investor who started SIP in 2015 and continued through 2020’s crash now has 158% cumulative returns. An investor who waited for “perfect market timing” with lump sum and is still waiting missed 124% cumulative gains.

Start now. Whether SIP or lump sum, start this week. Refine strategy later.

For most investors in today's market, the 60% SIP + 40% Lump Sum split is the most mathematically sound move.

Planning Beyond Accumulation: While this guide focuses on deploying capital through SIP

or lump sum, successful investors think decades ahead. If you're within 10 years of

retirement or already retired with a ₹50 lakh+ corpus, discover the best SWP mutual funds that generate ₹30,000-50,000 monthly income

while preserving your capital for 20-30 years.

SIP is better than lump sum for investors with regular monthly income, limited capital availability, or low market timing confidence. In 2025’s volatile yet trending market, an SIP in a Nifty 50 Index fund delivered 13.79% XIRR versus a lump sum’s 10.51% CAGR on a ₹10 lakh investment, performing better by 3.28%. This outperformance occurred because the SIP strategy successfully "bought the dips" during the market corrections in March and August 2025. However, "better" is highly subjective and depends entirely on your current financial situation and market entry point.

In 2025, a ₹10L Lump Sum grew to ₹11.05L (10.5% return), while a ₹83,333 SIP reached ₹11.38L (13.8% XIRR), winning by ₹33,000. While lump sum leads in steady bull runs, SIP captures 15% volatility dips, lowering break-even levels. Mathematically, lump sum wins long-term, but SIP offers superior peace of mind.

Switch anytime penalty-free.

Recommendation: Don't stop what’s working; layer new capital on top. Keep your ₹10K SIP for discipline and deploy a ₹5L bonus as a Lump Sum for immediate market participation. For falling markets, keep your original investment to avoid "loss crystallization" and start a new SIP to average down your entry price.

One missed payment is negligible, losing just ₹6,800 on a 10-year ₹10K SIP. However, three consecutive misses trigger auto-cancellation and a significant ₹92,000 compounding loss. Pro-Tip: If facing a cash crunch, reduce your SIP to the ₹500 minimum instead of stopping. It preserves your mandate and keeps the compounding clock ticking.

SIPs manage timing risk, not market risk. An equity SIP still carries equity volatility. In 2025, Nifty SIPs dipped 5.9% in March but recovered to 13.8% XIRR by year-end. Over 10+ year periods, Indian equity SIPs have historically shown 0% probability of negative returns. Safety comes from choosing Diversified/Large-cap funds and maintaining a 7-year+ horizon.

With Nifty at 25,703 (2.5% below peak), use a 70% SIP + 30% Lump Sum split. Start a ₹15,000 monthly SIP immediately. Keep your ₹3L Lump Sum in a Liquid Fund, deploying ₹1L chunks only on 5-8% market dips. This "Cushioned Entry" protects you from 2026 volatility while ensuring your capital isn't sitting idle.

Invest 30-50% of your monthly surplus. For an ₹80K income with ₹60K expenses, your target SIP is ₹6,000–₹10,000. To reach ₹50L in 15 years (12% return), you need exactly ₹10,040 monthly. The Golden Rule: A ₹5,000 SIP sustained for 10 years creates more wealth than a ₹20,000 SIP that you stop after 12 months.

A ₹10,000 SIP for 30 years at 12% creates ₹3.53 Crore. It makes you financially independent, not "billionaire rich." Starting at age 25 instead of 35 creates ₹2.3 Crore extra wealth. To maximize results, use a 10% Annual Step-Up, increasing your SIP as your salary grows can double your final corpus without feeling the pinch.