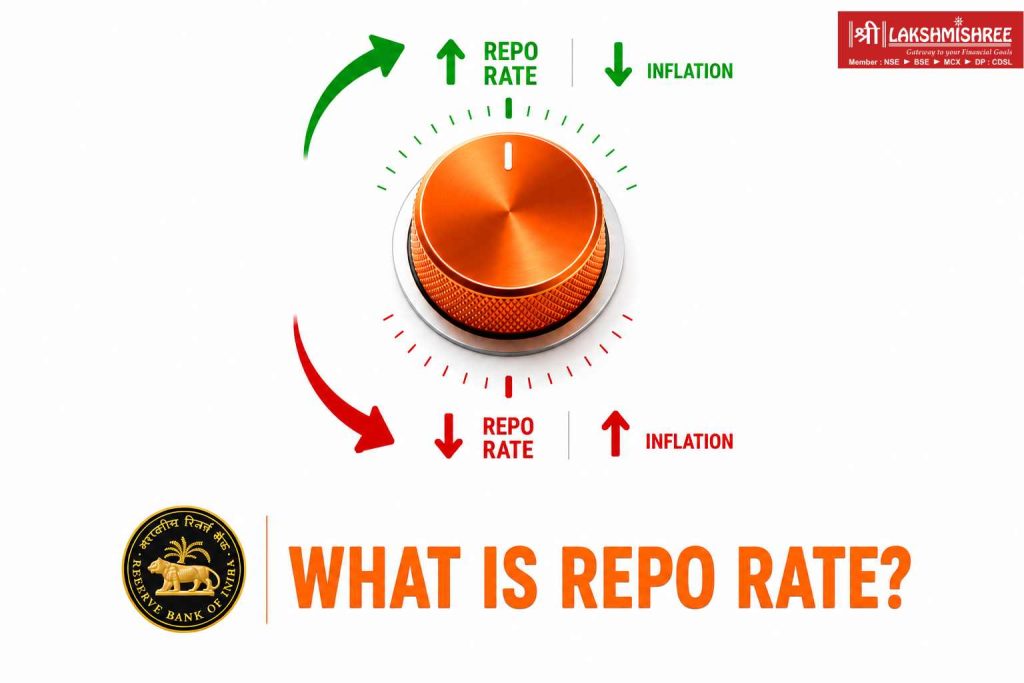

When the Reserve Bank of India wants to slow down inflation or push the economy to grow faster, the first tool it reaches for is the repo rate. Every MPC meeting, every rate cut or hike, all of it circles back to this one rate. And yet, most people who follow this news every two months have never really understood what is repo rate or what it actually does to their money.

This guide explains exactly that. What the repo rate is, how it works mechanically, why RBI changes it, and what it means for your home loan, your fixed deposit, and the stocks in your portfolio.

Related reading from this section: Reverse Repo Rate

Repo rate is short for Repurchasing Option Rate.

It is the interest rate at which the Reserve Bank of India lends short-term money to commercial banks. When a bank like SBI or HDFC needs funds urgently, it can borrow from the RBI by temporarily selling government securities to the central bank, with a promise to buy them back at a slightly higher price. The difference in that price, expressed as a percentage, is the repo rate.

Current repo rate (as of May 2026): 5.25%

Think of it this way: just as you pay interest when you borrow from a bank, banks pay interest when they borrow from the RBI. The repo rate is that interest.

The RBI reduced the repo rate by 25 basis points in December 2025, bringing it down to its current level. This followed a cumulative 125 basis points of cuts across FY2025-26. It is the most aggressive easing cycle since 2019.

Here is what actually happens during a repo rate transaction:

The entire process is designed to ensure banks never run out of liquidity while also giving the RBI a lever to control how much money flows through the system.

The Monetary Policy Committee (MPC) of the RBI, a six-member body chaired by the RBI Governor, meets every two months to review and set the repo rate. The key factors they weigh before finalising:

The decision on what is repo rate and what it should be is never based on just one factor. The MPC weighs all of these simultaneously. This is also the reason why rate decisions are sometimes surprising and always closely watched.

Join thousands of investors using Lakshmishree’s research to navigate the Indian markets with precision.

Understanding what is repo rate means recognizes that it does not operate in isolation. It sits at the centre of what the RBI calls the interest rate corridor, which is a band bounded by two other rates:

| Rate | Current Level | What It Means |

| MSF Rate (ceiling) | 5.50% | The rate at which banks can borrow in emergencies, pledging SLR securities |

| Repo Rate (centre) | 5.25% | The benchmark overnight lending rate |

| SDF Rate (floor) | 5.00% | The rate at which RBI absorbs excess liquidity from banks without collateral |

The SDF (Standing Deposit Facility) replaced the old reverse repo rate as the effective floor of this corridor in April 2022. This is worth understanding because most financial content still quotes the old reverse repo rate of 3.35%, which technically exists on the books but is no longer the operative rate. For a full explanation of the reverse repo rate and the SDF transition, see our [Reverse Repo Rate guide: SOON].

The 50-basis-point corridor SDF 25 bps below repo, MSF 25 bps above is how the RBI keeps short-term market rates anchored around the policy rate.

This is where the repo rate moves from abstract monetary policy and starts impacting your monthly bank statements.

Most home loans today are linked to the bank's Repo-Linked Lending Rate (RLLR), which moves in near-lockstep with the repo rate. When the RBI cuts the repo rate by 25 bps, your bank is required to pass on the change to floating-rate home loan borrowers. A 25 bps cut on a Rs 50 lakh loan with a 20-year tenure reduces EMI by approximately Rs 800–1,000 per month, or saves around Rs 2–3 lakh over the loan life.

These are also increasingly linked to external benchmarks. While the pass-through is not always immediate for non-home loans, a sustained rate-cutting cycle does bring consumer loan rates down over months.

A lower repo rate reduces the cost of working capital loans and term credit for businesses. This is why rate cuts are considered growth-supportive as they make it cheaper for businesses to borrow and expand.

The transmission is not always perfect or immediate. Banks sometimes delay passing on cuts, especially when they have older, fixed-rate liabilities. But over a full rate cycle, the repo rate is the most direct driver of the cost of credit in the economy.

Related Reading from this section: Top Government Banks India

The RBI's repo rate acts as the master lever of the economy, triggering a chain reaction that directly shifts the balance of returns across your entire investment portfolio.

Related Reading From This Section: Best SWP mutual fund plan to retire with monthly income

Understanding where the repo rate has come from helps contextualise where it is now.

| Period | Repo Rate | Context |

| 2014–2019 | 8.0% → 5.15% | Gradual easing under RBI Governors Rajan and Patel |

| 2020 (COVID) | Cut to 4.0% | Emergency cuts to support the economy |

| 2022–2023 | Raised to 6.5% | Aggressive hiking cycle to fight post-COVID inflation |

| 2024–2025 | 6.5% → 5.25% | Easing cycle as inflation came under control |

| Current (2026) | 5.25% | On hold, with debate on whether a hike cycle begins in FY27 |

The 2022–2023 hiking cycle was the sharpest since the 2010s. The RBI raised rates by 250 basis points in under 18 months to contain inflation that had surged past 7%. The subsequent easing cycle has been equally notable for its speed.

Related Reading From This Section: What is Non Performing Assets

While the repo rate dictates the cost of borrowing to inject funds into the economy, the reverse repo rate serves as the RBI's primary tool to absorb excess liquidity from the banking system.

| Feature | Repo Rate | Reverse Repo Rate |

| Direction | RBI lends to banks | Banks lend (deposit) to RBI |

| Current rate | 5.25% | 3.35% (officially; SDF rate of 5.00% is now operative) |

| Purpose | Injects liquidity into system | Absorbs excess liquidity from system |

| Collateral | Banks give govt securities | RBI gives govt securities (old mechanism) |

| Who benefits | Banks (get cheap funds) | RBI (mops up excess money) |

For the full breakdown of how these two rates interact and how the SDF has changed the picture, read our [Reverse Repo Rate guide].

The repo rate is the interest rate at which the Reserve Bank of India lends short-term funds to commercial banks against government securities under the Liquidity Adjustment Facility (LAF).

Key relationship: Higher repo rate → costlier bank borrowing → higher loan rates → reduced spending → lower inflation. Lower repo rate → cheaper credit → more lending → higher economic activity.

Ultimately, the Repo rate is the single most important pulse to track for any Indian investor. Whether you are paying off a home loan or building a long-term equity portfolio, every decision made by the Reserve Bank of India directly impacts your take-home wealth.

By understanding the mechanics of the current 5.25% benchmark and its relationship with the new SDF floor, you move beyond market guesswork and into the realm of research-led investing. As the RBI continues to balance inflation control with economic growth through 2026, staying informed will ensure your financial strategy remains resilient. Master the cycle, stay disciplined with your investments, and always align your portfolio with the shifting tides of monetary policy.

While the RBI repo rate drives market sentiment, high book value stocks provide a structural margin of safety. Protect your capital during interest rate shifts by targeting companies with a solid asset floor.

Join thousands of investors using Lakshmishree’s research to navigate the Indian markets with precision.

The current repo rate is 5.25%, as set by the RBI MPC in December 2025 and maintained through the April 2026 meeting.

The Monetary Policy Committee (MPC), comprising three RBI members including the Governor and three external members appointed by the government. Decisions require a majority vote.

The MPC meets every two months. Rate changes can happen at any meeting, though the RBI sometimes chooses to hold rates even if market expectations point toward a cut or hike.

Banks pay more to borrow from the RBI. They pass this on by raising lending rates. Credit becomes more expensive, consumption and investment slow, and inflation tends to fall over the following months.

While what is repo rate defines the interest banks pay to borrow from the RBI, the reverse repo rate is the interest the RBI pays banks to deposit their excess funds. The former injects cash into the economy; the latter absorbs it.

If your home loan is linked to the repo rate (RLLR), your EMI will not change instantly. Banks adjust it on your next scheduled loan reset date, which typically happens every 3 to 6 months (quarterly or semi-annually).

The core function of what is repo rate is to manage prices. By raising the rate, the RBI makes borrowing expensive. This reduces consumer spending and business borrowing, which cools down market demand and lowers inflation.

Yes, book your FD immediately. Banks lower their FD interest rates shortly after an RBI rate cut. Waiting means you will likely lock in a lower guaranteed return.

Banks pay it to borrow emergency or short-term cash from the RBI to maintain daily operational liquidity. They pledge government securities as collateral, and the repo rate is simply the interest they pay for that loan.