Every PSU stock screener in 2026 starts looking the same after a while. The big names have already been re-rated. Coal India at 2.47x book value. NMDC at 2.42x. BHEL at 5.14x. HAL at 8.27x. Most PSU stocks are no longer cheap on a balance-sheet basis, which is exactly why PSU penny stocks and high book value PSU stocks have started becoming much harder to find.

But while running through the BSE PSU Index data on Screener.in in May 2026, something interesting appeared beneath all that momentum: out of the 60 PSU stocks in the index, only 6 are still trading below book value (P/B < 1). And inside those six names is where the real conversation begins — a few are PSU penny stocks, a few are high book value PSU stocks, and a very small number satisfy both conditions simultaneously: PSU penny stocks with high book value.

That combination is rare in the current PSU market. This blog breaks the space into three simple lenses.

Category A focuses on high book value PSU stocks trading below book value (P/B below 1), where investors are effectively buying net assets at a discount; the purest traditional value-investing signal in the PSU space.

Category B focuses on PSU penny stocks with CMP below ₹200, making them accessible to retail investors working with smaller capital across the broader PSU universe.

Category C is where both filters meet simultaneously: PSU penny stocks with high book value, meaning stocks trading below ₹200 while also remaining below book value. As of May 2026, this is the rarest category in the entire BSE PSU Index.

Every number in this analysis comes directly from Screener.in’s live BSE PSU Index data pulled on May 5, 2026.

Related Reading section: High book value stocks in India | EV penny stocks with high book Value

| Category | What It Means | Filter Used | Stocks in This List | Best For |

| 🔵A | Book Value > CMP | P/B below 1.0 | Bank of Baroda, PNB, Union Bank, BoI, Central Bank, NIACL | Value investors seeking asset safety |

| 🟠 B | PSU Penny Stocks | CMP below ₹200 | Bank of Maharashtra, NMDC, NHPC, IOCL | Retail investors with small capital |

| 🟢 C | Both= Penny + Below Book | P/B < 1 AND CMP < ₹200 | Bank of India, Central Bank, PNB, Union Bank, NIACL | Best of both= value + accessibility |

The interesting part about PSU penny stocks with high book value in 2026 is not that they are cheap. The interesting part is that most PSU stocks are no longer cheap at all.

The 2022–2025 PSU re-rating completely changed the valuation landscape of the sector. Defence PSUs like HAL (P/B 8.27x), BEL (14.68x), and Mazagon Dock (10.87x) moved to valuation levels that would have looked unrealistic in 2020. Mining PSUs like Hindustan Copper touched 17.29x book value. Even traditional industrial names like BHEL re-rated to 5.14x book value during the cycle.

After a move like that, you would expect almost the entire PSU universe to be trading above book value.

But while screening the BSE PSU Index in May 2026, one pattern became difficult to ignore: most of the remaining book value discounts are concentrated in one sector- It is PSU banking.

That is why many of the remaining PSU penny stocks and high book value PSU stocks are banks.

The reason is not hidden. The market still carries the memory of the 2015–2018 NPA crisis. Even though PSU bank balance sheets have improved dramatically since then, valuation discounts continue to persist because investors still associate government-owned banks with slower governance structures, historical bad-loan cycles, and weaker digital perception compared to private sector banks like HDFC Bank (P/B 3.5x) and ICICI Bank (3.2x).

And that is precisely where the value-investing argument begins.

For a value investor, persistent pessimism is what creates the discount in the first place. The market already fully rewarded defence PSUs, railway PSUs, and several commodity PSUs during the re-rating cycle. PSU banking remains one of the few areas where valuation skepticism still survives.

At the same time, these stocks also happen to offer some of the lowest share prices in the broader BSE 500 universe, which is why PSU penny stocks with high book value characteristics increasingly overlap in 2026.

Out of the 60 companies in the BSE PSU Index, only a very small number now satisfy both conditions simultaneously: trading below ₹200 while also remaining below book value (P/B below 1). That rarity is what makes this segment interesting in the current market cycle.

For the complete list of PSU companies across all categories, see our PSU company list. For the governance structure behind Maharatna and Navratna PSUs, see our Navratna companies guide.

After screening all 60 companies in the BSE PSU Index in May 2026, only six PSU stocks remain trading below their book value per share (P/B below 1). In simple terms, the market is valuing these companies below the net asset value sitting on their balance sheets.

That alone is rare in the current PSU market cycle.

Most PSU stocks already participated aggressively in the 2022–2025 re-rating phase, with many names moving to 2x, 5x, and even 10x+ book value multiples. But these six companies still trade at a discount despite operating profitability, improving balance sheets, and continued government backing.

What makes the list even more interesting is that several of these names also qualify as PSU penny stocks, trading below ₹200 and remaining accessible to retail investors with smaller capital.

Every stock in this table passes three conditions simultaneously:

That combination is extremely uncommon in Indian equities. It means investors are simultaneously buying PSU stocks below their accounting value while still receiving dividend income during the waiting period for a possible valuation re-rating.

This is why PSU penny stocks with high book value characteristics remain one of the few surviving value-investing pockets inside the broader PSU universe in 2026.

All data from BSE PSU Index, Screener.in, May 5, 2026.

Standard filters often mislabel healthy PSU banks as "risky" because they mistake customer deposits for dangerous financial debt. Our adapted framework replaces the debt-to-equity filter with asset-quality metrics to reveal deep value while ensuring the balance sheet is genuinely safe.

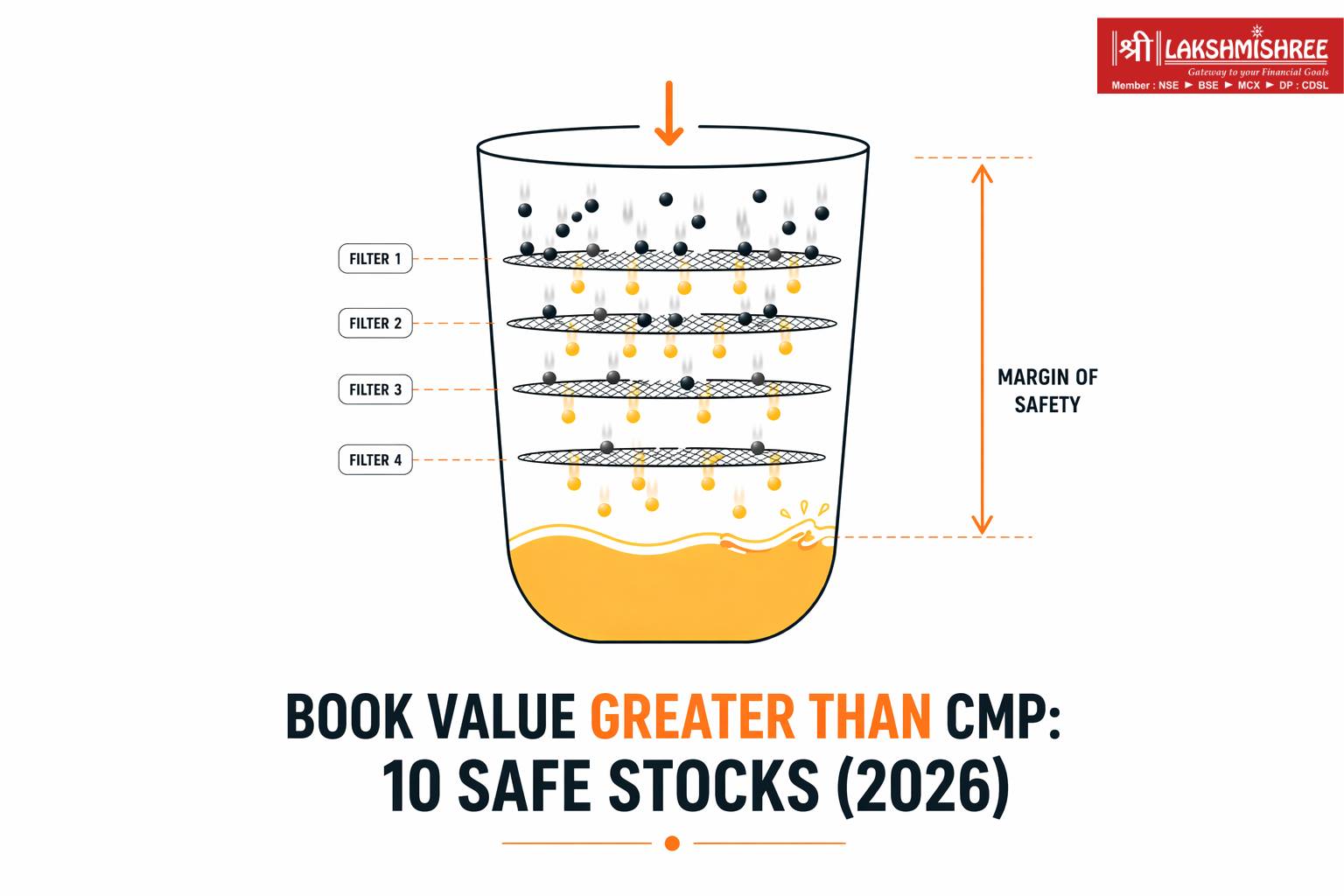

The standard Screener.in 5-filter framework for book value greater than CMP framework uses:

Book value > Current price AND Pledged percentage < 0.1% AND Market Capitalization > 200 AND Debt to equity < 1 AND Industry PE > Price to Earning

Contrastingly, for PSU banks specifically, the Debt/Equity < 1 filter does not apply. All banks carry deposits as liabilities by business model, which pushes D/E to 10x+ by default. The adapted framework for PSU banking stocks replaces D/E with:

Capital Adequacy Ratio (CAR) > 12% to confirm the bank can absorb further losses.

Gross NPA < 5% for asset quality threshold and

Provision Coverage Ratio > 65%: management has buffered against known bad loans

All the banking stocks in this list have been checked against these adapted filters. For the complete framework on reading NPA data before investing in any PSU bank, see our NPA guide.

A visual breakdown of how THIS BLOG uses 4+1 filters to remove risky and overvalued stocks, leaving only fundamentally strong, undervalued opportunities with a clear margin of safety.

| CMP | P/B Ratio | P/E Ratio | Div Yield | Market Cap |

|---|---|---|---|---|

| ₹138.25 | 0.73 | 6.17 | 2.93% | ₹62,940 Cr |

Among all 60 companies in the BSE PSU Index, Bank of India carries the deepest book value discount in May 2026. At a P/B ratio of 0.73x, the market is valuing the bank at just ₹73 for every ₹100 of net assets on its balance sheet.

That immediately places it among the most interesting PSU penny stocks with high book value characteristics still left after the broader PSU re-rating cycle.

Bank of India is a ₹62,940 crore PSU bank with nationwide and international operations, yet the stock continues trading at one of the lowest valuations in the PSU banking space. The discount largely comes from its historically high NPA burden and a slower recovery trajectory compared to peers like Bank of Baroda and Union Bank.

Still, the fundamentals are improving. The stock trades at a PE ratio of 6.17x, while the 19.16% one-year return suggests the market has started recognising the recovery story.

The bank continues passing key filters:

That combination places Bank of India firmly in Category C i.e. PSU penny stocks with high book value.

The risk is straightforward: the deepest discounts usually come with the highest uncertainty. Among PSU banking peers, Bank of India still carries concerns around slower NPA recovery, which is why the valuation discount persists.

For value investors, however, that uncertainty is also what creates the margin of safety.

| CMP | P/B Ratio | P/E Ratio | Div Yield | Market Cap |

|---|---|---|---|---|

| ₹35.74 | 0.83 | 7.24 | 1.69% | ₹32,349 Cr |

At ₹35.74, Central Bank is one of the lowest-priced stocks in the entire BSE PSU Index while still trading below its book value. That combination of low share price plus genuine asset discount makes it one of the clearest Category C PSU penny stocks with high book value characteristics in the market.

The stock currently trades at a P/B ratio below 1 and a PE of 7.24x, broadly in line with PSU banking peers. Meanwhile, the bank’s NPA profile has been improving and the Capital Adequacy Ratio (CAR) remains above RBI requirements.

What stands out, however, is the market’s indifference. The stock delivered a -3.34% one-year return even as the broader PSU sector rallied strongly. For value investors, that divergence is often the signal worth studying; improving fundamentals while market attention remains elsewhere.

The risk is equally visible. Central Bank has one of the smaller market caps among major PSU banks at around ₹32,349 crore, with lower institutional participation and thinner analyst coverage. That usually translates into slower re-rating cycles and higher uncertainty.

For investors screening PSU penny stocks in 2026, Central Bank remains one of the rare names where low price, improving fundamentals, and below-book valuation still exist together

| CMP | P/B Ratio | P/E Ratio | Div Yield | Market Cap |

|---|---|---|---|---|

| ₹108.40 | 0.84 | 7.01 | 2.66% | ₹1,24,583 Cr |

PNB is a ₹1.24 lakh crore PSU bank trading at around ₹108 per share. It is a rare combination where a large-cap bank still qualifies as both a PSU penny stock and a below-book-value stock.

That combination is unusual in Indian equities. Most companies above ₹1 lakh crore market capitalisation typically trade well above 1.5x book value, yet PNB continues trading below its balance-sheet value even after the broader PSU re-rating cycle.

The discount largely comes from the market’s lingering memory of the 2018 Punjab National Bank fraud case. Even though the bank’s balance sheet and profitability have improved materially since then, the valuation still carries a governance discount compared to private sector peers.

Fundamentally, however, the recovery is visible. PNB trades at a PE ratio of 7.01x versus many private banks trading closer to 20–25x earnings multiples. The bank continues paying dividends, while the 9.34% one-year return suggests gradual market re-rating is already underway.

What makes PNB especially important in this list is liquidity. Compared to smaller PSU banks like Central Bank or Bank of India, PNB offers much easier entry and exit for investors seeking PSU banking exposure with below-book-value characteristics.

For investors looking at PSU penny stocks with high book value potential, PNB remains one of the most practical large-cap options available in 2026.

| CMP | P/B Ratio | P/E Ratio | Div Yield | Market Cap |

|---|---|---|---|---|

| ₹264.30 | 0.83 | 7.01 | 3.16% | ₹1,36,679 Cr |

Bank of Baroda is not technically a PSU penny stock at around ₹264 per share, sitting above the ₹200 threshold. But among all PSU banks trading below book value, it stands out as one of the highest-quality institutions in the list.

The stock trades at a P/B ratio of 0.83x and a PE ratio of 7.01x, creating a rare double-undervaluation signal i.e. cheap on both assets and earnings simultaneously.

Unlike smaller PSU banks still fighting credibility concerns, Bank of Baroda already operates as a structurally stronger franchise. The bank has international operations across 17 countries, an improving NPA trajectory, and management quality that strengthened significantly after the merger with Dena Bank and Vijaya Bank.

The 3.16% dividend yield is also among the highest in the PSU banking cluster, adding income support while investors wait for further valuation re-rating.

For investors who want below-book-value PSU banking exposure without moving too far down the risk curve, Bank of Baroda remains one of the strongest quality-versus-valuation combinations available in the PSU sector in 2026.

Our Government banks in India comparison cover Best Government Banks India for investors across different metrics.

| CMP | P/B Ratio | P/E Ratio | Div Yield | Market Cap |

|---|---|---|---|---|

| ₹162.80 | 0.94 | 6.39 | 2.92% | ₹1,24,275 Cr |

Union Bank trades closest to book value in this list at a P/B ratio of 0.94x, but it compensates with the strongest one-year return in the entire PSU banking discount cluster at 29.76%.

That combination matters because it signals something unusual: momentum layered on top of value. The market is already beginning to recognise the recovery story while the stock still trades below its balance-sheet value.

The bank also trades at a PE ratio of 6.39x, the lowest in this peer group, while offering a dividend yield of 2.92%. Compared to deeper-discount names like Bank of India or Central Bank, Union Bank appears further along in the re-rating cycle.

That creates an important distinction for investors. If PSU bank valuations continue improving, Union Bank may be one of the first names in this list to cross above the P/B 1 threshold, meaning the window for buying below book value could close faster here than in other PSU penny stocks with high book value characteristics.

For investors prioritising momentum plus valuation support, Union Bank stands out as one of the strongest combinations in the PSU banking space in 2026. Those seeking deeper balance-sheet discounts, however, may still prefer Bank of India’s larger margin of safety at 0.73x book value.

| CMP | P/B Ratio | P/E Ratio | Div Yield | Market Cap |

|---|---|---|---|---|

| ₹161.85 | 0.92 | 22.35 | 1.11% | ₹26,672 Cr |

New India Assurance is the only PSU stock in the index outside the banking sector that trades below book value. It is India's largest general insurance company by gross written premium backed by the government of India and trades at ₹161 against a book value significantly above that price.

The PE of 22.35x is higher than the banking stocks in this list, reflecting insurance sector dynamics rather than earnings weakness. The one-year return of -5.22% has created the discount. The underlying business general insurance is structurally growing as Indian vehicle, health, and property insurance penetration expands.

Adding NIACL to a PSU portfolio alongside PSU banks provides sector diversification. All other below-book PSU stocks in this list are banking or banking-adjacent. NIACL is insurance a different economic cycle, different regulatory risk, different earnings driver.

| CMP | P/B Ratio | P/E Ratio | 1Yr Return | Market Cap |

|---|---|---|---|---|

| ₹78.60 | 1.83 | 8.61 | +53.09% | ₹60,455 Cr |

Bank of Maharashtra does not qualify as a below-book-value PSU stock at a P/B ratio of 1.83x, but at around ₹78 per share it remains one of the most accessible PSU banking stocks in the market.

What stands out is the momentum. The stock delivered a 53.09% one-year return i.e. the strongest performance in the entire PSU banking peer group as the market aggressively re-rated the bank following one of the fastest NPA recovery cycles among PSU banks.

This makes Bank of Maharashtra a Category B stock: a PSU penny stock by price, but not by book value discount.

The investment case here is different from names like Bank of India or Central Bank. The focus is not deep asset undervaluation but continued earnings growth and operational improvement.

The key risk is valuation. Much of the easy re-rating already happened once the NPA recovery became visible. From here, future upside depends more on sustained earnings performance and slippage control rather than simple valuation expansion.

| CMP | P/B Ratio | Div Yield | ROCE | Market Cap |

|---|---|---|---|---|

| ₹89.43 | 2.42 | 3.68% | 29.59% | ₹78,625 Cr |

NMDC is India’s largest iron ore producer and one of the strongest non-bank PSU penny stocks in the BSE PSU Index. At around ₹89 per share, it remains highly accessible despite the PSU re-rating cycle pushing its valuation to a P/B ratio of 2.42x.

Unlike the PSU banks in this list, NMDC’s strength comes from operational quality rather than deep book value discounting.

The standout numbers are exceptional for a commodity company: ROCE of 29.59%, debt-to-equity of just 0.11, and a dividend yield of 3.68%. After the 2022 demerger of NMDC Steel, the parent company became a cleaner pure-play iron ore miner with one of the strongest balance sheets in the PSU universe.

What makes NMDC important in this list is diversification. Most PSU penny stocks are concentrated in banking and insurance, while NMDC adds exposure to mining and commodities with significantly higher capital efficiency than most PSU banks can deliver.

For investors seeking PSU penny stocks beyond financials, NMDC remains one of the highest-quality options available in 2026.

| CMP | P/B Ratio | P/E Ratio | Div Yield | Market Cap |

|---|---|---|---|---|

| ₹83.13 | 2.03 | 26.43 | 2.30% | ₹83,504 Cr |

NHPC is India’s largest hydropower PSU and one of the most accessible non-bank PSU penny stocks in the market at around ₹83 per share.

Unlike the below-book PSU banks in this list, NHPC’s investment case is based on asset quality rather than asset discount. The company owns hydropower infrastructure with extremely long operational lifespans, low running costs, and relatively predictable regulated tariff income.

The stock trades at a P/B ratio of 2.03x, meaning the market already assigns value to the quality and durability of its assets. Meanwhile, the 2.30% dividend yield provides steady income while holding.

The recent -1.60% one-year return has created a modest cooling-off phase after the broader PSU rally, giving investors a more reasonable entry point compared to peak optimism levels.

The key risk is valuation. NHPC trades at a PE ratio of 26.43x, one of the highest in this list, meaning future growth expectations are already partially priced in. The next phase of upside depends on successful execution and commissioning of new hydropower projects.

| CMP | P/B Ratio | P/E Ratio | Div Yield | Market Cap |

|---|---|---|---|---|

| ₹141.20 | 1.02 | 5.58 | 4.96% | ₹1,99,391 Cr |

IOCL is the borderline case in this list. At a P/B ratio of 1.02x, it trades fractionally above book value rather than below it. But at around ₹141 per share, a PE ratio of just 5.58x, and a dividend yield of 4.96%, it remains one of the strongest income-focused PSU penny stocks in the market.

As India’s largest oil refiner and fuel marketer, IOCL processes nearly 80 million metric tons of crude oil annually. The recent -4.24% one-year return and near-book valuation reflect uncertainty around crude prices and government-managed fuel pricing, both of which can pressure refining margins.

What makes IOCL stand out is income yield. No other PSU penny stock in this list offers a dividend yield close to 5% at this price level.

For investors building a PSU portfolio focused on cash flow and dividend income rather than deep book value discounts, IOCL remains one of the most practical options available in 2026.

Most of the below-book-value PSU stocks in this list belong to banking or insurance. Current PSU bank NPA ratios improved significantly after the 2018 crisis, but that recovery happened during a strong credit cycle. Any deterioration in MSME or agriculture loan quality could pressure both earnings and book values again.

The government continues reducing stakes in PSU companies to meet SEBI’s 25% public shareholding requirement by August 2026. Large OFS (Offer for Sale) supply entering the market can temporarily suppress stock prices even when fundamentals improve.

One of the biggest mistakes investors make with PSU penny stocks is assuming low P/B automatically leads to re-rating. Many PSU banks have traded below book value for years. A stock at 0.83x book value can remain there for a long time without a strong catalyst like NPA improvement, earnings acceleration, or governance changes.

Patience is not optional in PSU value investing. The discount only matters if the underlying business continues improving while the market remains slow to recognise it.

Step 1: Go to screener.in → search "BSE PSU" → click the BSE PSU Index page.

Step 2: Click the CMP/BV column header to sort by Price-to-Book ascending. All stocks below 1.00x appear at the top, these are your book value discount PSU stocks.

Step 3: For PSU penny stocks, look for the CMP column and mentally filter for anything below ₹200. You will immediately see Central Bank (₹35), UCO Bank (₹26), IOB (₹34), Bank of Maharashtra (₹78), SJVN (₹79), NHPC (₹83), NMDC (₹89), IRFC (₹104), PNB (₹108), Canara Bank (₹134), Bank of India (₹138), IOCL (₹141).

Step 4: Cross-reference with the NPA data in quarterly results for banking stocks. The Screener.in company page for each bank shows historical NPA ratios and provision coverage in the financial data section.

Step 5: For the adapted PSU bank filter, run this query directly in Screener.in's query box:

Book value > Current price AND Market Capitalization > 10000

AND Price to Earning < 15 AND Dividend yield > 2This surfaces the quality PSU banks with genuine book value discount and income support simultaneously.

India’s PSU penny stocks in 2026 reveal something the headline indices do not: genuine book value discounts still exist inside the government-owned universe, concentrated mostly where the market remains cautious- PSU banking.

Out of 60 companies in the BSE PSU Index, only a handful still trade below book value, and an even smaller group combines that discount with penny-stock accessibility. That rarity is what makes these stocks interesting.

But the important thing about PSU penny stocks with high book value characteristics is that they rarely reward impatience.

They reward the investor willing to sit with discomfort while the market looks elsewhere. Not the one chasing the latest IPO or momentum rally, but the one who runs the screen, studies the balance sheet, tracks NPA recovery, checks capital adequacy ratios, and waits for valuation gaps to close over time.

That kind of patience used to be called value investing.

In 2026, it is increasingly rare, which is exactly why the opportunity still exists.

Bank of India at P/B 0.73 is the deepest book value discount in the entire 60-stock BSE PSU index. You are buying ₹100 of net banking assets for ₹73. Among non-banking PSUs, ONGC at P/B 1.00 is the closest to book value parity in the energy sector.

As of May 2026, 12 PSU index stocks trade below ₹200: UCO Bank (₹26), IOB (₹34), Central Bank (₹35), Bank of Maharashtra (₹78), SJVN (₹79), NHPC (₹83), NMDC (₹89), IRFC (₹104), PNB (₹108), Canara Bank (₹134), Bank of India (₹138), and IOCL (₹141).

The perfect combination of P/B below 1 AND CMP below ₹200 — exists in five BSE PSU stocks: Bank of India (₹138, P/B 0.73), Central Bank (₹35, P/B 0.83), PNB (₹108, P/B 0.84), Union Bank (₹162, P/B 0.94), and New India Assurance (₹161, P/B 0.92). These five are simultaneously discounted to book value and accessible at penny prices.

The 2022–2025 PSU re-rating pushed the majority of PSU stocks: defence, mining, power, infrastructure to P/B multiples of 2x to 17x. The BSE CPSE Index delivered 26.1% CAGR over five years. The stocks that remained below book value are concentrated in PSU banking, where NPA legacy and governance concerns continue to apply a discount despite fundamentally improving metrics.

NMDC at ₹89 is below ₹100 in price but trades at P/B 2.42x above book value. The investment case is not book value safety but earnings quality: ROCE of 29.59%, D/E of 0.11, and dividend yield of 3.68% make it the highest-quality non-bank PSU penny stock in the index. You pay a premium to book value for quality of returns, not for asset safety.

NPA analysis for PSU bank investment is a complete framework in itself. Our dedicated NPA guide covers gross NPA vs net NPA, provision coverage ratio, slippage ratio, and the 5-point investor checklist for any PSU bank investment decision.

| What you want to explore | Where to go |

|---|---|

| Full PSU company list by category | PSU Company List India |

| Navratna and Maharatna PSU governance | Navratna Companies in India |

| Book value > CMP 5-filter framework | Book Value Greater Than CMP |

| High book value stocks across all sectors | High Book Value Stocks India 2026 |

| PSU bank analysis | Government Banks in India |

| Understanding NPA before investing | What is NPA? |

| Open Demat to invest in PSU stocks | Open Account with Lakshmishree |

Disclaimer: This article is for educational and informational purposes only. It does not constitute investment advice or a recommendation to buy or sell any securities. All data is sourced directly from the BSE PSU Index page on Screener.in as of May 5, 2026 and is subject to real-time change. Verify all figures independently before making investment decisions. Investments in the securities market are subject to market risks. Consult a SEBI-registered financial advisor before investing. Lakshmishree Investment & Securities Ltd. — SEBI Regn. No.: INZ000170330 | Research Analyst: INH000014395.

© 2026 Lakshmishree Investment & Securities Ltd. All rights reserved.