Published: March 11, 2026 | Reading Time: 12 minutes |

Most retirees run out of money not because they spent too much, but because they chose the wrong withdrawal strategy. Fixed deposits are a slow leak draining your wealth through taxes. In contrast, the best SWP plan can be a method you can actually control: same income, zero tax, all while your Corpus grows.

Think it’s complicated?

Well, it’s not. Let this guide reveal the exact SWP funds Lakshmishree retirees use, the 4% withdrawal rule that ensures your monthly Income lasts 30+ years, and the tax loophole that keeps ₹12,000-15,000 of your money annually in your pocket instead of the government’s.

10-Year Mathematical Divergence

A Systematic Withdrawal Plan (SWP) is a mutual fund facility that lets you withdraw a fixed amount monthly, quarterly, or annually from your investment. Unlike FD interest or fund dividends, you control the withdrawal amount and timing, paying lower capital gains tax instead of income tax.

When you withdraw ₹50,000 through an SWP, the government treats it as a proportional redemption of your assets. Roughly ₹44,650 is a return of your own original capital (100% Tax-Free), and only ₹5,350 is considered profit or gains. In Year 1, if your fund grew 12%, (₹6,000-8,000 of your ₹50,000 monthly withdrawal might be taxable gains. After the ₹1.25 lakh annual exemption, your tax becomes ₹0 for the first 2-3 years.

Fixed deposits tax your entire interest as income. SWP taxes only the profit portion and gives you an exemption on top.

While FD interest is taxed at 30% for high earners, SWP capital gains are taxed at 12.5% but only on gains above ₹1.25 lakh annual exemption. For a ₹6 lakh annual withdrawal (₹50K/month), typical Year 1 tax: ₹0 to ₹5,000 vs ₹12,750 in FD.

That’s ₹7,750-12,750 saved. Every single year.

Let’s compare ₹1 crore corpus for monthly income:

In Year 6-10, when your SWP corpus has grown to ₹1.18-1.25 crore despite withdrawals, you can increase your monthly income to ₹55,000-60,000 to match inflation. If you choose FD as a retiring partner, it would still be stuck at ₹45,583 with purchasing power eroded by 25-30%.

Think again. Here’s what the math actually shows:

Measuring a 7-Year window under 6% Inflation

In 7 years, your ₹45,583 payout will stay the same, but it will only buy what ₹30,312 buys today.

Because your corpus grows, you can scale your payout to ₹65,000–₹70,000 to match inflation while keeping your capital intact.

For the best SWP plans in India, hybrid/balanced advantage funds work perfectly because they blend equity (12-15% returns) with debt (stability). Top choice: HDFC Mid Cap Fund with 24 % 3-year returns, medium risk, and dynamic allocation that protects your withdrawals during market corrections.

Institutional Performance & Direct Onboarding

Selecting a leader is the first step. Structuring it for a Systematic Withdrawal Plan is how you protect your lifestyle. Learn which of these funds are best for SWP.

Selection Criteria: when choosing best SWP plans in India, ensure 3-year trailing returns >14%, volatility (standard deviation) <12%, AUM >₹5,000 Cr for liquidity, expense ratio <1.5%, consistent performance across bull and bear markets.

"Inflation at 6% is a silent killer of Fixed Deposits. While SWP protects your cash flow, your actual 'Safe Haven' assets need a different strategy.

Compare: Gold vs. Silver Investment Strategy for 2026

The 4% rule states that withdrawing 4% of your corpus annually (₹4 lakh from ₹1 crore, or ₹33,333 monthly) ensures your money lasts 30+ years even through market corrections. This safe withdrawal rate balances income needs with corpus preservation across retirement.

A 1998 study (Trinity Study, updated through 2020) tested withdrawal rates across 50+ year periods.

Results:

Most Lakshmishree SWP clients use 6-7% withdrawal rates successfully because:

6% annual withdrawal (₹6 lakh/year = ₹50,000/month on ₹1 crore) with annual review. Reduce to 4-5% if corpus drops >15% in a year. Increase to 7-8% if corpus grows >₹1.15 crore.

4% Sustainable Growth vs. 8% Capital Exhaustion

Assumption: 10% average annual fund return, both scenarios.

An extra ₹33,333/month (₹4L annual) for 10 years gives you ₹40 lakh more income. But you’ve depleted your corpus by ₹65 lakh. In Year 11-25, you’re scrambling with a dying corpus while the 4% withdrawer is still collecting ₹50,000+ monthly from a ₹1.5 crore portfolio.

Average withdrawal rate: 6.2%

Average corpus: ₹78 lakh

Average monthly income: ₹40,000

Clients who reduced corpus below starting value (10 years): 12%

Clients who grew corpus despite withdrawals (10 years): 68%

What about the 20% in between? Basically flat, which is still fine as they got their monthly income and preserved capital.

SWP taxation: Only capital gains are taxed, not the entire withdrawal. For equity funds held over 1 year, Long-Term Capital Gains (LTCG) up to ₹1.25 lakh annually are tax-free. Beyond that, 12.5% tax applies only to the gain portion of your withdrawal.

Mr. Kashyap's SWP example: after analysing all the best SWP plans for MR. Kashyap, we recommended -₹1 crore in HDFC Balanced Advantage Fund, growing at 12% annually, ₹50,000 monthly SWP (₹6 lakh annual withdrawal).

Of the ₹6 lakh withdrawn, how much is capital gain of MR. Kashyap? ?

Typically, Year 3-4, when Mr. Kashyap's accumulated gains exceed the ₹1.25L exemption. Even then:

Compare to FD: ₹7 lakh interest (on ₹1 Cr @ 7%) taxed at 30% = ₹2,10,000 annual tax.

The Best SWP plans save you ₹1,95,000+ annually from Year 3 onwards.

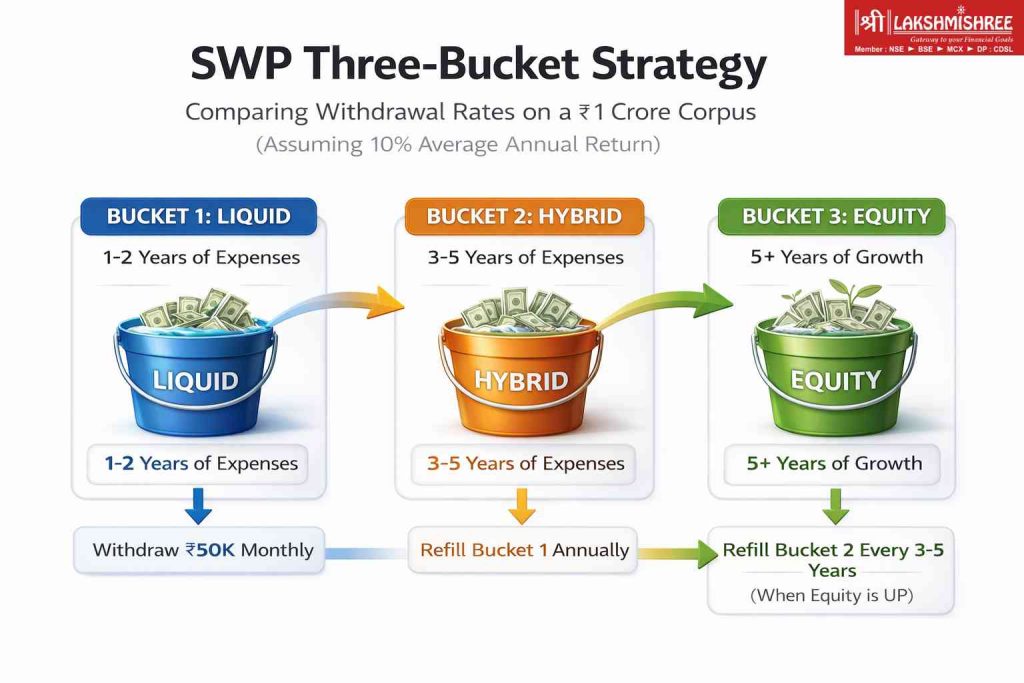

The three-bucket strategy divides your corpus into liquid (1-2 years expenses), hybrid (3-5 years), and equity (5+ years) buckets. Withdraw from liquid first, refill from hybrid annually, refill hybrid from equity every 3-5 years. This protects against selling equity in crashes.

In 2020’s March crash, equity funds dropped 30-35%. If you were withdrawing directly from equity, you’d be selling at the bottom and locking in losses.

With three buckets? Your Bucket 1 (liquid) had 2 years of expenses. You didn’t touch equity for 24 months. By March 2022, equity recovered fully. You refilled Bucket 1 from Bucket 2 (hybrid, which only dropped 15%), then refilled Bucket 2 from Bucket 3 (equity) in 2023 when markets were at all-time highs.

Result: You withdrew ₹12 lakh (₹50K × 24 months) from liquid funds while equity recovered. Then sold equity at peak to refill. Never sold equity at a loss.

Sounds complicated? Here is a simple version to understand:

Most investors implement a "two-bucket lite” version: 70% in one hybrid fund (HDFC Balanced Advantage), 30% in liquid fund. Withdraw from liquid. Refill liquid from hybrid once a year. Simple, effective, protects 90% of the downside.

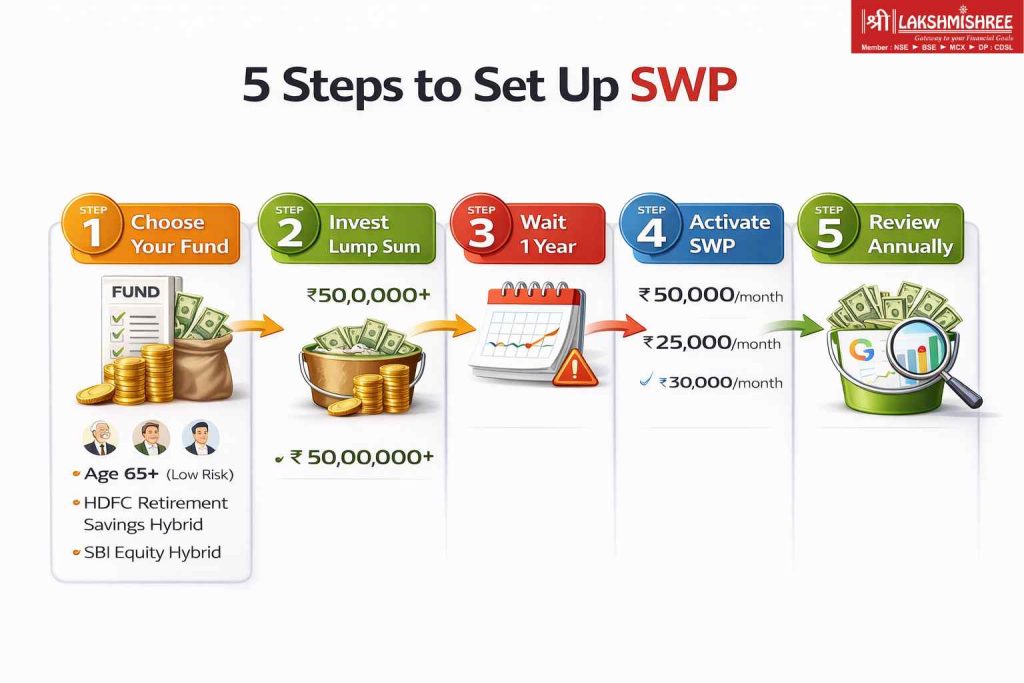

To set up best SWP plans in India:

(1) Choose hybrid fund based on your age/risk,

(2) Invest lump sum,

(3) Wait 366 days for LTCG tax benefit,

(4) Activate SWP with 6-7% annual withdrawal rate,

(5) Review annually and adjust if corpus changes >15%.

The process takes 10 minutes online.

Step-by-step:

This is where most people mess up:

If you start SWP before 366 days, you pay Short-Term Capital Gains (STCG) tax at 20%. After 1 year, Long-Term Capital Gains (LTCG) at 12.5% with ₹1.25L exemption.

₹6 lakh annual withdrawal, 100% STCG (before 1 year):

Same withdrawal, LTCG (after 1 year):

Wait. The. Full. Year.

During this year, your fund grows. ₹1 crore @ 12% = ₹12 lakh gain. You’re starting SWP with ₹1.12 crore corpus, not ₹1 crore.

Every March, check:

The error: Investing ₹1 crore in March 2025, starting SWP in April 2025 (Month 2).

The damage: Entire withdrawal taxed as STCG @ 20% instead of LTCG @ 12.5%. On ₹6L annual withdrawal with ₹60K gain, you pay ₹12,000 tax instead of ₹0.

The fix: Mark your calendar for 366 days from investment date. Start SWP on Day 367, not before. Even if you need income immediately, take from savings for Year 1—the ₹12,000 tax saving is worth it.

The math: ₹1 crore corpus, ₹8 lakh annual withdrawal (₹66,666/month).

Why it fails: Even at 10% fund returns, you’re eroding corpus 8% and earning 10% = net +2% annually. After inflation (6%), you’re shrinking in real terms. By Year 15, corpus drops to ₹60-65 lakh. By Year 20, you’re scraping by on ₹30-40 lakh.

The fix: Stick to 6-7% max. ₹50,000-58,000/month on ₹1 crore. If you need ₹66,666/month, you need a ₹1.15 crore corpus, not ₹1 crore.

The scenario: March 2020 crash. Your ₹1 crore corpus drops to ₹85 lakh (equity portion crashed 35%). You continue ₹50,000/month withdrawal.

What happens: You’re now withdrawing 7% annually (₹6L from ₹85L) instead of 6%. This accelerates depletion. Worse, you’re selling equity units at the bottom when NAV is depressed—getting fewer rupees per unit redeemed.

The fix:

The trap: You’re 72 years old, still in Kotak Equity Hybrid (70% equity allocation).

The risk: A 2008-style crash (equity -50%) drops your ₹1 crore to ₹65 lakh. You don’t have 10 years to wait for recovery. You need that monthly income to live.

The fix:

Lakshmishree's recommendation: HDFC Balanced Advantage auto-adjusts equity/debt based on valuations, handles this for you.

The assumption: “I have ₹0 tax, so I don’t need to file ITR.”

The problem: IT department sees ₹6 lakh annual credits to your bank account. No ITR showing source = notice asking “where did this money come from?”

The fix: File ITR every year, even if tax is ₹0. Show SWP redemptions under Schedule “Capital Gains.” Shows:

Takes 10 minutes using Lakshmishree. Saves potential ₹10,000-50,000 penalty notice hassle.

Rajesh Sharma, 62, invested ₹85 lakh in HDFC Balanced Advantage Fund in February 2023. Started ₹45,000/month SWP in March 2024. After 24 months (March 2026), withdrew ₹10.8 lakh total, paid ₹0 tax, corpus grew to ₹89.2 lakh, a net ₹4.2 lakh gain.

The full story:

Client Profile:

What Lakshmishree Recommended (February 2023):

Why HDFC Balanced Advantage?

Results (March 2024 → March 2026, 24 months):

Financial Outcome:

Equivalent FD Scenario:

₹85 lakh FD @ 7% interest:

SWP vs FD Comparison:

| Factor | FD | SWP | Winner |

|---|---|---|---|

| Total income (2 years) | ₹11,90,000 | ₹10,80,000 | FD (+₹1.1L) |

| Tax paid (2 years) | ₹1,19,000 | ₹0 | SWP (saves ₹1.19L) |

| Net income after tax | ₹10,71,000 | ₹10,80,000 | SWP (+₹9,000) |

| Corpus after 2 years | ₹85,00,000 | ₹89,20,000 | SWP (+₹4.2L) |

| Total advantage | — | — | SWP (+₹4.29L) |

Key Lesson:

6.35% withdrawal rate (₹5.4L annual on ₹85L corpus) was sustainable because:

At Lakshmishree, we’ve set up SWP plans for retirees across the nation through our Mumbai, Varanasi, and Surat offices. Our process:

We understand:

We recommend 1-3 funds based on your profile:

We set calendar reminder for Day 366. On that day:

Call: 0542-6600000

Email: [email protected]

Visit expected: Mumbai (Lower Parel) | Varanasi | Surat

Visit: lakshmishree.com/

Fill 2-minute form

Get callback within 30 minutes (9 AM - 7 PM)

You now understand why the best SWP plans in India aren’t fixed deposits—they’re hybrid mutual funds that give you tax-free income, corpus growth, and inflation protection.

The question isn’t whether to use SWP. The question is: how many more years will you let ₹12,750 slip away to taxes when ₹0 is possible?

Here’s what you know now that 95% of retirees don’t:

1. The 4% Rule: Withdraw 4-6% annually (₹50,000/month from ₹1 crore), and your corpus lasts 30+ years, even grows.

2. The Tax Loophole: LTCG exemption up to ₹1.25 lakh means ₹0 tax for the first 2-3 years on ₹6 lakh annual withdrawals.

3. The Right Funds: HDFC Balanced Advantage Fund (18.2% returns), ICICI Equity & Debt (16.8%), Aditya Birla Balanced Advantage (17.5%). These aren’t random picks. They’re proven performers with 10+ year track records.

4. The 366-Day Rule: Wait one full year before starting SWP. This single decision saves you 20% STCG tax versus 12.5% LTCG tax worth ₹10,000-15,000 annually.

5. The Three-Bucket Strategy: Withdraw from liquid funds during market crashes, refill from equity when markets recover. Never sell at the bottom.

But knowledge without action is just expensive entertainment.

SWP analysis based on March 2026 fund data. Past performance doesn’t guarantee future returns. Tax calculations assume LTCG holding (>1 year) and 12.5% tax above ₹1.25 lakh exemption per current tax laws. Actual tax depends on individual slab, fund performance, regulatory changes. 3-year returns are trailing annualized as of February 28, 2026. Fund rankings based on risk-adjusted returns (Sharpe ratio), consistency, and AUM liquidity.

This is educational content, not personalized investment advice. Consult SEBI-registered advisor (Lakshmishree Investment and Securities, SEBI Registration No. INZ000170330 ) before investing. Mutual funds subject to market risk. Read scheme documents carefully before investing.

HDFC Balanced Advantage Fund is ranked #1 for SWP in India with 18.2% 3-year returns, medium risk, ₹5,000 minimum investment, and dynamic equity-debt allocation. It provides stable monthly withdrawals by automatically reducing equity exposure during overvalued markets and increasing during corrections.

SWP withdrawals are taxed as capital gains. For equity mutual funds held over 1 year, Long-Term Capital Gains (LTCG) tax is 12.5% on gains exceeding ₹1.25 lakh annual exemption. With ₹50,000/month withdrawal, first 2-3 years typically have ₹0 tax due to exemption and cost recovery.

Yes, for three reasons:

Tax efficiency: Dividends taxed as income at your slab (up to 30%). SWP taxed as capital gains at 12.5% LTCG with ₹1.25L exemption.

Control: You decide withdrawal amount and frequency. Dividend: fund decides.

NAV impact: Dividend payout reduces NAV. SWP: you redeem units, but remaining units keep growing.

Example: ₹1 crore corpus needs ₹6L annual income.

Dividend option: Fund declares 6% dividend = ₹6L. Taxed @ 30% = ₹1.8L tax. NAV drops proportionally.

SWP: You withdraw ₹6L via redemption. Only ~₹1.5-2L is taxable gain (after ₹1.25L exemption) @ 12.5% = ₹10-15K tax.

Savings: ₹1.65-1.75 lakh annually.

SWP continues regardless of NAV. If NAV falls, more units are redeemed for the same withdrawal amount, accelerating corpus depletion. Mitigation: Choose balanced/hybrid funds with 40-60% debt cushion, reduce withdrawal 10-20% during severe corrections, or pause SWP temporarily using emergency savings.

Yes, the SWP amount is fully flexible. Cancel existing SWP instruction and set a new amount, takes 1 business day with no penalty. Common reasons: income needs increased, pension started (reduce SWP), market correction (temporary pause), or corpus growth (increase amount).

Duration depends on fund returns. At 10% annual return with ₹50,000/month SWP (6% withdrawal rate), corpus lasts 25+ years and ends at ₹1.8 crore. At 8% return, 20+ years. At 12% return, perpetual—corpus keeps growing despite withdrawals. Conservative estimate: 20-25 years sustainability.

The math:

Scenario 1: 10% Fund Return, ₹50K/Month (6% Withdrawal)

Year 5: ₹1.08 crore (grew despite ₹30L withdrawn)

Year 10: ₹1.18 crore (withdrew ₹60L total)

Year 15: ₹1.29 crore (withdrew ₹90L total)

Year 20: ₹1.42 crore (withdrew ₹1.2 crore total)

Year 25: ₹1.56 crore (withdrew ₹1.5 crore total)

Scenario 2: 8% Fund Return, ₹50K/Month (6% Withdrawal)

Year 5: ₹1.02 crore (slight growth)

Year 10: ₹1.06 crore (still growing)

Year 15: ₹1.08 crore (slowing)

Year 20: ₹1.07 crore (plateau)

Year 25: ₹1.02 crore (still intact)

Scenario 3: 12% Fund Return, ₹50K/Month (6% Withdrawal)

Year 10: ₹1.48 crore

Year 20: ₹2.19 crore

Year 30: ₹3.24 crore

Perpetual: Grows forever, even with withdrawals