You're here because you saw two terms. IPO and FPO. They sound similar, and they both involve companies raising money. Both happen in the stock market. But here's what you need to know right now: An IPO is when a company sells shares to the public for the first time. An FPO is when an already listed company sells more shares to raise additional funds.

That's it. That's the core difference.

But if you stop reading now, you'll miss something crucial. You see, understanding IPO vs FPO isn't just about definitions. It's about knowing which one to invest in, when to invest, and why companies choose one over the other. It's about avoiding the mistakes that cost investors lakhs of rupees. And it's about recognizing opportunities that others miss because they never looked beyond the surface.

This confusion brought you here. It Is Good. Because by the time you finish this guide, you'll understand not just IPO and FPO, but also FPO vs OFS, QIP, rights issues, and exactly how each one affects your investment decisions. You'll know which carries less risk. You'll understand the regulatory frameworks. And you will recognize patterns that separate smart investors from those who simply follow the crowd.

Think of this as your final stop for IPO vs FPO clarity. Everything you need, nothing you don't.

Related Reading: What is HNI in IPO | QIP in IPO

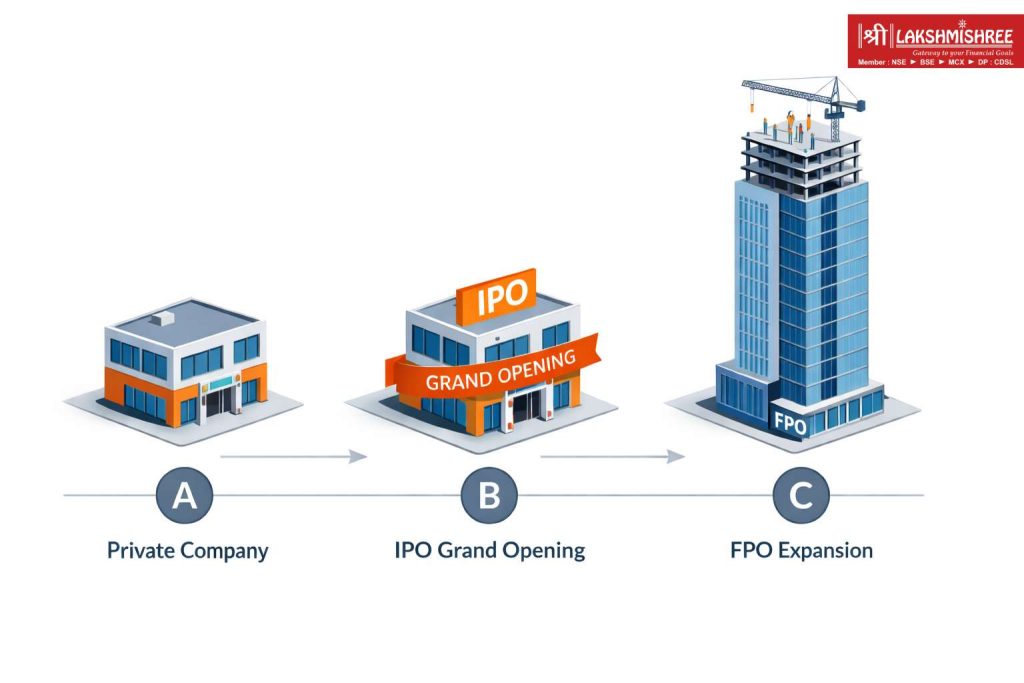

IPO stands for Initial Public Offering.

It's a company's grand entrance. The moment a private company becomes public. The day promoters decide to share ownership with everyday investors like you.

Here's what happens: A private company—let's say it's been operating for years, growing steadily, building its business, decides it needs capital. Big capital. Maybe to finance expansion operations. Maybe to pay off debt. Maybe to fund acquisitions. Whatever the reason, the promoters choose to go public.

They hire investment bankers. File mountains of paperwork with SEBI (Securities and Exchange Board of India). Get their books audited, scrutinized, questioned. Then they price their shares and offer them to the public for the very first time.

This is the IPO.

When you subscribe to an IPO, especially a fixed price IPO, you're buying shares of a company that has never been publicly traded before. There's no historical share price. No trading volume. No liquidity in the secondary market yet. You're taking a leap of faith based on the company's fundamentals, its prospectus, and the price band set by the underwriters.

Real Example: When Zomato launched its IPO in July 2021 at ₹76 per share, it was the first time retail investors could own a piece of India's food delivery giant. Before that, only venture capitalists and private equity firms could invest. The IPO raised ₹9,375 crore and gave Zomato the public market access it needed to compete with rivals.

Every company does not necessarily go public. There are a few very legitimate reasons why a Company chooses to go public, or in other words, why a company launches an IPO.

There's a strategy involved. There is a calculation(a lot of it). Risk assessment. Here's why promoters pull the IPO trigger:

FPO stands for Follow-on Public Offering.

Notice the word "follow-on." It comes after the IPO. It's the sequel, to the original IPO.

When a company is already listed on stock exchanges and already trading publicly, already followed by analysts, already owned by thousands of shareholders—it can come back to the market to raise more money. This is an FPO.

The company already has a share price. Market capitalization. Trading history. Quarterly results. Analyst coverage. Everything that an IPO lacks, an FPO has.

Real Example: In 2020, Yes Bank launched an FPO to raise ₹15,000 crore. Yes Bank was already a household name, already trading on stock exchanges since 2005. But it needed capital to recover from a financial crisis and meet regulatory capital requirements set by the RBI. So it issued fresh shares through an FPO, not an IPO.

Related Reading from this section: top performing PSU bank shares

The Two Faces of FPO: Dilutive type vs. Non-Dilutive type

Not all FPOs are created equal. There are two distinct types, and the difference matters tremendously to investors:

The company issues new shares. This increases the total number of shares outstanding. Your existing shareholding percentage gets diluted (reduced), but the company gets fresh capital to use for growth, debt reduction, or expansion.

Effect on existing shareholders: Your ownership percentage drops, but if the company uses the capital wisely, the share price may rise, offsetting the dilution.

Existing shareholders, usually promoters or large investors, sell their shares to the public. No new shares are created. The company doesn't receive any money. Instead, the selling shareholders cash out.

Effect on existing shareholders: No dilution in ownership percentage, but it signals that existing stakeholders want to exit (which may or may not be a red flag depending on context).

Here's where it gets interesting: Many FPOs combine both types. The company issues fresh shares AND promoters sell some of their holdings simultaneously. You need to read the offer document carefully to understand the mix.

To understand IPO and FPO better we will bisect these two in one table. We should see in this section how IPOs and FPOs are different in many ways. Let's put them side by side.

| Parameter | IPO (Initial Public Offering) | FPO (Follow-on Public Offering) |

|---|---|---|

| Definition | First-time public sale of shares | Additional sale of shares by an already listed company |

| Company Status | Private company going public | Already listed public company |

| Share Price History | None - price is set via book building | Existing market price provides reference |

| Risk Level | Higher - no trading history | Lower - established track record |

| Information Available | Limited to prospectus and pre-IPO data | Years of quarterly results and analyst reports |

| Pricing Mechanism | Book building or fixed price method | Usually at a discount to current market price |

| SEBI Scrutiny | Extremely rigorous documentation | Regulated but based on existing track record |

| Lock-in Period | Yes, for anchor investors and promoters | May vary depending on structure |

| Purpose | Transition to public, raise capital | Raise growth capital or promoter exit |

| Example | Zomato, Paytm | YES Bank |

Notice something? FPOs are generally less risky than IPOs.

Why? Because you have data. Years of financial performance. Market validation. Trading liquidity. When you invest in an FPO, you know the company's earning patterns, its management quality, its competitive positioning. With an IPO, you're betting on potential.

But, and this is crucial, as less risk also means less explosive upside potential. IPOs can double on listing day (or crash 20%). FPOs rarely do that because the market has already priced the company.

Let's address this quickly because it comes up constantly:

Both are part of the primary market—where companies raise fresh capital directly from investors. This is different from the secondary market, where you and I trade existing shares on NSE and BSE.

Related reading: What is primary market and secondary market

Here's where things expand.

IPO and FPO aren't the only ways companies raise money. Smart investors know the full menu but which companies raise money. Let's explore:

OFS is specifically for promoters or large shareholders to sell their stakes. No new shares. No fresh capital for the company. Just an ownership transfer.

IPO vs FPO vs OFS:

QIP is an FPO's sophisticated relative or cousin. In finance, instead of offering shares to the general public, the company sells to qualified institutional buyers (QIBs), for example, mutual funds, insurance companies, foreign portfolio investors.

Related Reading: Understand QIP before investment

IPO vs FPO vs Rights Issue:

Wait, NFO? That's not for companies. It's for mutual funds. When a new mutual fund scheme launches, it's called an NFO. You're buying units of the fund, not shares of a company. Entirely different.

This is the question, is it not?

You want a definitive answer. You want to hear things like, "Always invest in FPOs" or "IPOs are superior." But here's the truth: it depends.

You might not like that answer. But let us explain why it depends, and then you will have a framework to decide for yourself.

Invest in IPOs when:

Invest in FPOs when:

Neither is inherently better. IPOs offer higher potential returns but come with higher risk and less information. FPOs offer stability, data, and transparency but may not deliver explosive gains. Your choice depends on:

Here's where we stop being academic and get practical.

At Lakshmishree Investment & Securities Ltd. With 31 years of experience, we have been guiding investors through IPOs and FPOs since the previous century. We're not just another brokerage we're a SEBI-registered corporate member of NSE, BSE with over 60000+ investors who we help to make informed decisions.

Here's what we offer:

Related reading in this section: ASBA facility- your money stays in your bank until allotment.

Let's bust some myths regarding the IPO and FPO.

Reality: Many IPOs list below issue price. Paytm's IPO in 2021 listed at ₹1,950 against an issue price of ₹2,150 - a 9.3% loss on day one. LIC's mega IPO in 2022 also listed below issue price.

Listing gains are not guaranteed. They depend on market conditions, valuations, and demand-supply dynamics.

Reality: YES Bank's FPO in 2020 was meant to rescue the struggling bank. Investors who subscribed hoping for safety lost money as the stock continued to decline post-FPO.

FPOs can fail too. Especially if the company is in distress.

Reality: Quality over quantity. Applying blindly to every IPO is a recipe for capital destruction. Research each opportunity. Understand the business. Compare valuations. Only then invest.

Reality: If you've read this far, you know this is completely wrong; the finance implications and strategies differ greatly between IPOs and FPOs. IPO is the debut; FPO is the encore. Different stages, different risks, different information availability.

Let Us give you a checklist. Practical. Actionable. Use this every time you

evaluate a IPO or FPO.

Before Investing in an IPO, Ask:

✓ Does the company have a unique competitive advantage?

✓ Are promoters retaining significant skin in the game (>60% post-IPO)?

✓ Is the business model profitable, or at least has a clear path to profitability?

✓ Are valuations reasonable compared to listed peers?

✓ Is the IPO priced for long-term growth or short-term hype?

✓ What are the risk factors disclosed in the prospectus?

✓ Who are the anchor investors? (Quality matters)

✓ What will the company do with IPO proceeds?

Before Investing in an FPO, Ask:

✓ Why does the company need more capital now?

✓ Is it a fresh issue (company gets money) or OFS (promoters exit)?

✓ How has the stock performed in the last 1-3 years?

✓ Are quarterly results improving or declining?

✓ Is the FPO priced at a discount to market price?

✓ What is analyst consensus on the stock?

✓ Is promoter holding increasing or decreasing through this FPO?

✓ Will the dilution impact EPS significantly?

If you can't answer these questions confidently, don't invest. Simple as that.

SEBI doesn't just regulate; it aims to protect. Here's how the regulatory framework

ensures fairness:

For IPOs:

SEBI's role is crucial. But remember: regulation ensures process integrity, not investment success.

Due diligence is still your responsibility.

Related Reading : HNI Full Form, Meaning & How to Apply as HNI in an IPO

Let's lock this in once again and for the last time.

IPO (Initial Public Offering):

FPO (Follow-on Public Offering):

OFS (Offer for Sale):

Think of it this way:

All three happen in the primary market. All three are SEBI-regulated. But the intent, structure, and investor implications are different.

We have read a lot of theory regarding IPO vs FPO. But let's look at actual examples from Companies which are the talk of the town.

Background: Zomato, India's leading food delivery platform, launched its IPO in July 2021 at ₹76 per share. The company raised ₹9,375 crore.

IPO Details:

What happened next: The stock soared to ₹169 within months, then crashed below ₹50 during the 2022 market correction. As of 2026, it trades around ₹185, validating long-term believers but punishing short-term speculators.

Lesson: IPOs can be volatile. If you believed in Zomato's long-term story and held through the volatility, you won. If you chased listing gains and sold at ₹50, you lost.

Suggested reading from this Section: Mukesh Ambani startup investments

Background: Yes Bank, once a high-flying private lender, launched a massive FPO in July 2020 to raise ₹15,000 crore to rebuild its capital base following a regulatory rescue.

FPO Details:

What happened next: The stock faced heavy pressure due to the massive supply of new shares (equity dilution). While it helped the bank survive and meet regulatory capital requirements, the share price remained stagnant for years, testing the patience of retail investors.

Lesson: FPOs from companies in distress can be "equity heavy." Even if the business survives, the sheer number of new shares can prevent the stock price from rising quickly in the short term.

Background: Paytm launched India's largest-ever IPO at ₹2,150 per share, raising ₹18,300 crore.

IPO Details:

What happened next: The stock crashed to below ₹500 within a year. Investors lost 75%+ of their capital. It became one of India's biggest IPO disasters.

Lesson: Valuations matter. Hype doesn't. If an IPO is priced too aggressively and fundamentals don't justify it, stay away.

Let's talk money and numbers. Specifically, how much you keep versus how much you pay the government.

| Feature | Short-Term (STCG) | Long-Term (LTCG) |

|---|---|---|

| Holding Period | Up to 12 months | More than 12 months |

| Tax Rate | 20% | 12.5% |

| Exemption | None (Fully taxable) | First ₹1.25 Lakh per year is free |

| Listing Gains? | Usually STCG (20%) | N/A |

Related Reading from this section: LTCG Vs STCG Taxation in India

Let us make this simple.

Step 1: Open a Demat Account

You need a Demat account to hold shares electronically. At Lakshmishree, opening an account takes 5 minutes online.

Start Your Demat Account Application →

Step 2: Link Your Bank Account

Use UPI or net banking for instant, seamless payments. Your money stays in your account until shares are allotted (ASBA mechanism).

Step 3: Check IPO/FPO Calendar

We publish upcoming IPOs and FPOs on our platform. Read our research reports. Understand the opportunity.

Step 4: Apply Online

Step 5: Track Allotment

Check allotment status on the registrar's website or through our platform. If allotted, shares credited to your Demat account. If not, refund processed automatically.

Step 6: Decide Your Strategy

Hold for long-term wealth creation or trade on listing day—your call. We provide post-listing research to guide your decision.

Need help? Our relationship managers are available to assist. Call us or chat online.

More Resources On IPO : Knowledge base On IPO

SEBI publishes investor awareness content. Here are the key warnings:

Let's peer ahead.

India's IPO market is booming. In 2025 alone, over ₹1.5 lakh crore was raised through IPOs. FPOs, while less frequent, remain crucial for companies needing growth capital.

Trends to watch:

What this means for you: More opportunities, but also more noise. The ability to separate good IPOs from hyped ones will determine your returns. Lakshmishree's research team stays ahead of these trends. We analyze every IPO and FPO, providing you with unbiased, data-driven insights.

Let's bring it all together.

IPO vs FPO isn't a battle. It's a choice. A choice informed by your goals, your risk appetite, and the specific opportunity in front of you.

IPOs offer excitement. The thrill of being early. The potential for explosive returns. But they come with information gaps, volatility, and the risk of overpaying for hype.

FPOs offer stability. Years of track record. Market validation. Lower risk. But they may not deliver the adrenaline rush or the multibagger returns that IPOs occasionally do.

The smart investor's approach?

Diversify across both. Allocate a small portion of your portfolio to carefully researched IPOs. Invest in FPOs when fundamentally strong companies offer value. Don't put all your eggs in one basket.

And most importantly: Do your homework. Read prospectuses. Analyze financials. Understand the business. Don't blindly follow tips.

You came here confused about IPO vs FPO. You're leaving with clarity. You know the definitions, the differences, the risks, the opportunities, and the frameworks to make smart decisions.

That's the Lakshmishree promise. We don't just execute trades; we educate investors.

Ready to start your investment journey?

Open your Demat account with Lakshmishree today and get access to:

IPO is a company's first public sale of shares, while FPO is when an already-listed company sells additional shares. IPO transitions a private company to public; FPO raises more capital for an existing public company.

FPOs are generally safer because the company has a proven track record, years of financial data, and established market presence. IPOs carry higher risk due to lack of historical performance data.

Yes. Both are open to retail investors. You need a Demat account and sufficient funds to apply.

FPO can include fresh issue (company gets capital) or OFS (existing shareholders sell), or both. OFS specifically means no new shares are created—only existing ones change hands.

Shares are credited to your Demat account within T+3 working days of the issue closing (as per SEBI norms). Refunds for non-allotment are processed within 10 days.

QIP (Qualified Institutional Placement) is a faster way for listed companies to raise funds by selling shares only to institutional investors, not retail. FPO is open to all investors.

Both are part of the primary market, where companies raise capital directly from investors. The secondary market (NSE, BSE) is where existing shares are traded between investors.

Yes. Once shares are listed on stock exchanges, you can sell them immediately. However, remember that short-term gains are taxed at 20%.

If an IPO receives less than 90% subscription, it's considered a failure and the entire amount is refunded. FPOs also face similar scrutiny, though requirements may vary.

Compare the company's price-to-earnings (P/E) ratio with industry peers. Read analyst reports. Check if promoters are selling heavily. If valuations seem disconnected from fundamentals, it's likely overpriced.

Disclaimer: This article is for educational purposes only and should not be construed as investment advice. IPO and FPO investments carry market risks. Please read all offer-related documents carefully and consult with a financial advisor before investing. Past performance is not indicative of future results.

Published by Lakshmishree Investment & Securities Ltd. | CIN: U74110MH2005PLC157942 | SEBI Registration: INZ000170330