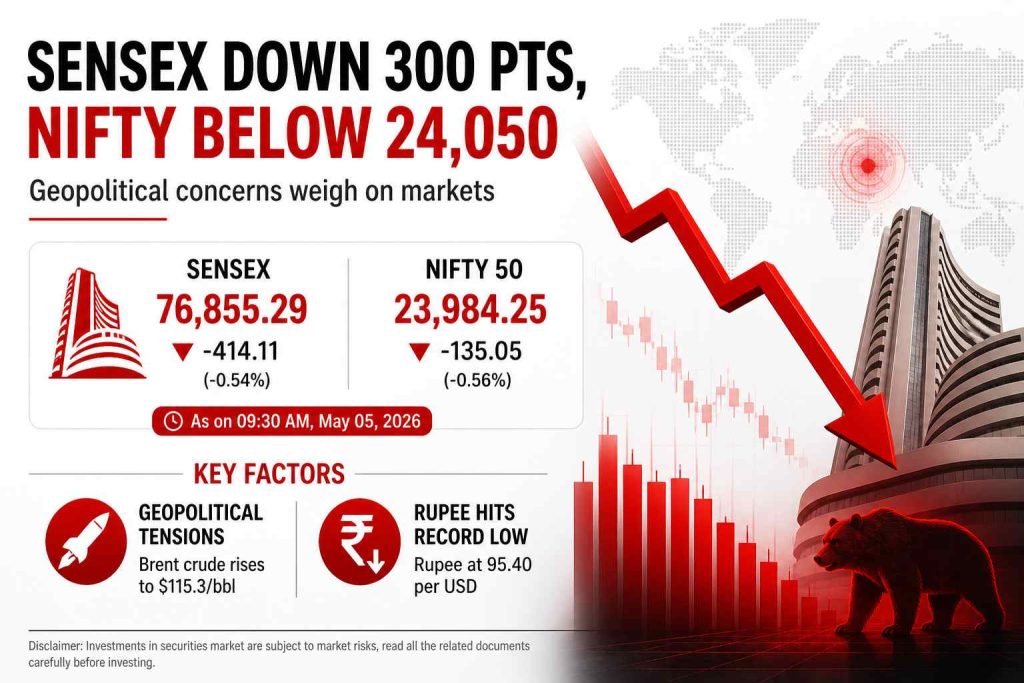

Indian equity markets opened on a weak note on Tuesday, with benchmark indices extending losses as global and macroeconomic pressures intensified. The Sensex declined 414 points to 76,855, while the Nifty fell below the crucial 24,000 mark to 23,984, reflecting a clear shift toward risk-off positioning.

The decline was primarily driven by escalating geopolitical tensions in the Middle East. Brent crude surged to an intraday high of $115.3 per barrel after Iran intensified attacks in the region, including disruptions around the strategically critical Strait of Hormuz. For an economy like India, heavily dependent on oil imports, this sharp rise in crude prices raises immediate concerns around inflation, fiscal pressure, and corporate cost structures.

Adding to the pressure, the Indian rupee weakened to a record low against the US dollar. Currency depreciation in such an environment not only increases import costs but also dampens foreign investor sentiment, particularly at a time when global risk appetite remains fragile. The combination of rising oil prices and a weakening currency creates a dual macro headwind for domestic equities.

Sectoral trends reflected this caution. Banking and financial stocks remained under pressure, given their sensitivity to liquidity and macroeconomic stability, while other cyclical sectors also witnessed selling. The broader market lacked strong defensive support, indicating that investors were focused more on reducing exposure than rotating capital.

Market participants are also closely watching global bond yields and foreign institutional investor (FII) flows. Elevated US yields continue to limit capital inflows into emerging markets like India, adding another layer of constraint to any near-term recovery.

In essence, the market is reacting to a convergence of external risks rather than domestic weakness alone. Geopolitical instability, elevated crude prices, and currency depreciation are collectively shaping sentiment and driving near-term price action.

While the decline does not yet indicate a structural reversal, it underscores the sensitivity of current market levels to global developments. Until there is clarity on geopolitical tensions and stabilization in crude and currency markets, volatility is likely to remain elevated, with downside risks persisting in the short term.

Kaashika is a social media strategist and financial content creator at Lakshmishree. She specialises in simplifying complex IPO and stock market concepts into clear, easy-to-understand content. Having created over 500+ pieces of financial content across reels, blogs, website posts and digital creatives, Kaashika helps audiences connect with the world of finance in a more accessible and engaging way.