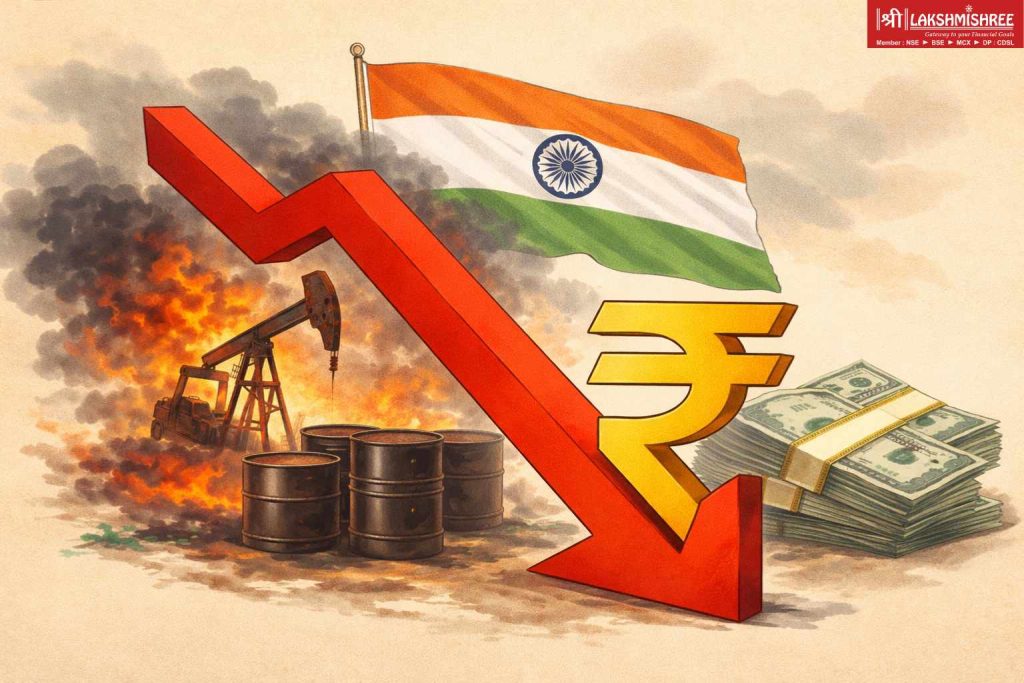

The ongoing conflict in West Asia is beginning to expose the vulnerability of the Indian rupee, as rising oil prices and global uncertainty weigh heavily on the currency’s outlook. The rupee recently touched a record low of 92.47 against the US dollar, highlighting growing concerns about India’s external stability.

Since the start of the Iran conflict, the rupee has weakened by about 1.5 percent, underperforming several Asian peers. In comparison, the Chinese yuan has slipped only marginally, while the Singapore dollar has shown relatively stronger resilience, reflecting differences in economic buffers and exposure to oil shocks.

The sharp rise in crude oil prices up nearly 40 percent since the conflict began—is emerging as the key pressure point for India. As one of the world’s largest oil importers, India faces a direct hit to its import bill, inflation outlook and current account balance when energy prices rise. This dynamic is now being reflected in currency markets.

Global banks have started adjusting their strategies accordingly. Market participants report that institutions are increasingly recommending cross-currency trades, positioning for further weakness in the rupee against currencies like the Chinese yuan and Singapore dollar. The view is that economies with stronger export performance, larger reserves and better insulation from oil shocks are likely to outperform.

Analysts point out that China, for instance, benefits from strong export momentum and substantial crude reserves, which provide a cushion against energy volatility. Similarly, expectations of tighter monetary policy in Singapore are seen as supportive for its currency, especially in managing imported inflation.

Beyond oil, the rupee is also facing pressure from weak portfolio flows, a widening non-oil trade deficit and slowing IT export growth, all of which are limiting its ability to withstand global shocks.

Market participants are treading cautiously, with hedge funds and institutional investors reducing exposure amid rising volatility. While relative trades between stronger and weaker currencies remain in focus, risk appetite has declined, keeping positions limited.

The broader takeaway for investors is clear: the Iran war is not just an energy story—it is increasingly becoming a currency and capital flow story, with uneven impacts across emerging markets. For India, the combination of high oil dependence and external vulnerabilities is placing the rupee under sustained pressure in the near term.

Kaashika is a social media strategist and financial content creator at Lakshmishree. She specialises in simplifying complex IPO and stock market concepts into clear, easy-to-understand content. Having created over 500+ pieces of financial content across reels, blogs, website posts and digital creatives, Kaashika helps audiences connect with the world of finance in a more accessible and engaging way.