Keypoints:

- RBI intervention triggered short-term relief: The rupee jumped to 93.59 after the RBI capped banks’ currency positions, forcing unwinding of large speculative trades and driving dollar selling.

- Underlying pressure remains strong: Despite the rebound, the rupee is still down over 4% due to high oil prices, foreign outflows and a strong dollar, indicating no real fundamental recovery.

- Spillover into markets and economy: A weak rupee is feeding into stock market losses, inflation risks and corporate cost pressures, keeping overall investor sentiment cautious and volatile.

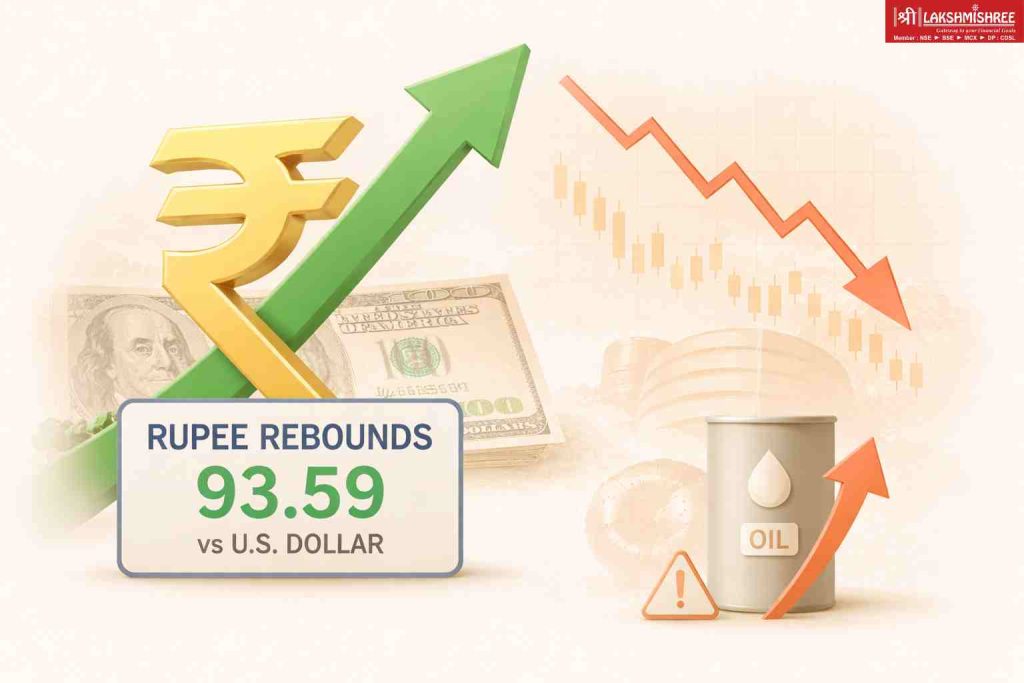

The Indian rupee staged a sharp recovery on Monday, opening 130 paise higher at 93.59 against the U.S. dollar after the Reserve Bank of India (RBI) moved to curb speculative activity in the currency market. The rebound comes after the rupee had slipped to a record low of around 94.85 last week, highlighting the growing stress in India’s financial system amid global uncertainty, March 30, 2026.

The central bank directed all banks to limit their net open positions in the rupee to $100 million in the onshore market, with compliance mandated by April 10. This measure is aimed at reducing large speculative bets against the currency and stabilising sharp fluctuations. As a result, banks and traders have begun unwinding arbitrage positions built between onshore and offshore markets, triggering a wave of dollar selling and lifting the rupee in early trade.

Market participants estimate that positions worth billions of dollars may need to be squared off in the coming days, creating short-term support for the currency. However, analysts caution that this recovery is largely technical in nature and does not reflect a fundamental improvement in the rupee’s outlook.

The broader trend remains weak. Since the escalation of the Iran conflict in late February, the rupee has depreciated by more than 4 percent, making it one of the worst-performing Asian currencies. The decline has been driven by a combination of rising crude oil prices, persistent foreign portfolio outflows and a strengthening U.S. dollar.

For India, which is heavily dependent on oil imports, elevated crude prices have a direct impact on the currency. Higher import bills widen the current account deficit and increase demand for dollars, putting sustained pressure on the rupee. At the same time, global investors have been pulling money out of Indian equities, further weakening capital flows.

The impact is already visible across financial markets. On Monday, equity benchmarks extended their losses, with the Sensex falling over 1,100 points and the Nifty 50 slipping below the 22,500 mark in early trade. The sell-off wiped out nearly ₹7 lakh crore in market capitalisation, reflecting heightened risk aversion among investors.

The interplay between currency and equity markets is becoming increasingly evident. A weaker rupee raises input costs for companies, especially those reliant on imports, which in turn affects profitability and investor sentiment. It also contributes to inflationary pressures, as higher fuel costs feed into transportation and consumer prices.

The RBI has been actively intervening in both onshore and offshore currency markets in recent weeks to slow the pace of depreciation. The latest move to cap bank positions represents a more direct attempt to control speculative flows and restore stability. While it has provided immediate relief, the effectiveness of such measures will depend on how global conditions evolve.

For investors, the current environment signals caution. The rupee’s rebound may ease immediate concerns, but it does not alter the broader challenges facing the economy. Currency weakness, volatile oil prices and uncertain global cues continue to shape market behaviour.

In essence, the situation reflects a market driven less by domestic fundamentals and more by external forces. As long as geopolitical tensions remain elevated and energy prices stay high, both the rupee and equity markets are likely to remain volatile.

The near-term outlook, therefore, remains fragile. Short-term recoveries may offer brief relief, but sustained stability will depend on a combination of easing global tensions, softer oil prices and a revival in capital inflows. Until then, investors are likely to navigate a landscape marked by sharp swings and cautious sentiment.

Kaashika is a social media strategist and financial content creator at Lakshmishree. She specialises in simplifying complex IPO and stock market concepts into clear, easy-to-understand content. Having created over 500+ pieces of financial content across reels, blogs, website posts and digital creatives, Kaashika helps audiences connect with the world of finance in a more accessible and engaging way.